At the top of the market, quant hiring is brutally selective. Acceptance rates at firms like Jane Street and Citadel are often below 5%, and memorized interview prep fails 80 to 90% of candidates once an interviewer changes the problem slightly, according to this quant interview analysis.

That changes how serious candidates should think about how to become a quant. This isn’t a career you drift into with a few Python notebooks and a vague interest in markets. Firms hire for evidence: mathematical depth, coding fluency, research judgment, and the ability to work under pressure when the problem has no clean template.

The positive side is that the route is more defined than it appears. The downside is that much of the guidance found online is either overly academic or lacks depth. Effectiveness comes from a practical roadmap that aligns with how firms screen candidates, what hiring managers care about, and where specialized recruiters can help candidates avoid wasting months on the wrong roles.

Table of Contents

- What a Quant Really Does and Why It Is So Competitive

- Building Your Academic and Mathematical Foundation

- Mastering the Quant Technical Stack

- Creating a Portfolio That Gets You Noticed

- Navigating the Quant Job Hunt and Interview Gauntlet

- Your First Year as a Quant and Beyond

What a Quant Really Does and Why It Is So Competitive

A quant isn’t one job. It’s a cluster of jobs that sit close to trading, research, data, and infrastructure.

The confusion starts because candidates use one label for very different roles. A quant researcher designs signals, tests hypotheses, studies market structure, and decides whether a model has enough edge to deserve capital. A quant developer builds the systems that make research usable in production, including data pipelines, backtesting engines, execution logic, and performance tooling. A quant trader sits closer to risk, monitoring, and strategy oversight, often deciding when a model should be trusted, throttled, or turned off.

That distinction matters because each path rewards different strengths. A strong stochastic calculus background helps in research. Systems thinking and performance optimization matter more in development. Decision-making under uncertainty matters more in trading.

Practical rule: Candidates who say they want to be “a quant” usually lose ground until they can explain which quant job they actually want.

Much public content portrays the field as cinematic. In truth, the work is narrower and tougher. Most days involve cleaning data, checking assumptions, reviewing failed tests, debugging code, and rejecting weak ideas. The glamour is overstated. The standards aren’t.

The real source of competition

The competition isn’t only about pay or prestige. It’s about the mix of skills required in one person.

Firms want people who can reason mathematically, code cleanly, understand noisy data, and stay rigorous when results are ambiguous. That combination is rare. Even good candidates often have one major gap. Some can solve probability problems but can’t write production-quality code. Others can build excellent software but don’t know how to test a market hypothesis without fooling themselves.

A useful way to calibrate expectations is to read a concrete algorithmic trader job description. It quickly shows how broad the bar is in practice: research logic, technical implementation, market awareness, and operational discipline all show up in one hiring profile.

What firms actually reward

Top firms don’t reward effort alone. They reward signal.

That means a candidate gets noticed for things like:

- Research clarity: Can the candidate explain why a strategy might work before opening a notebook?

- Technical precision: Can the candidate implement it without leaking future information or creating a fragile pipeline?

- Statistical judgment: Can the candidate tell the difference between a real effect and a lucky backtest?

- Communication under pressure: Can the candidate defend assumptions when pushed?

People who understand this early prepare differently. They stop chasing broad finance content and start building the exact mix of evidence the market pays for.

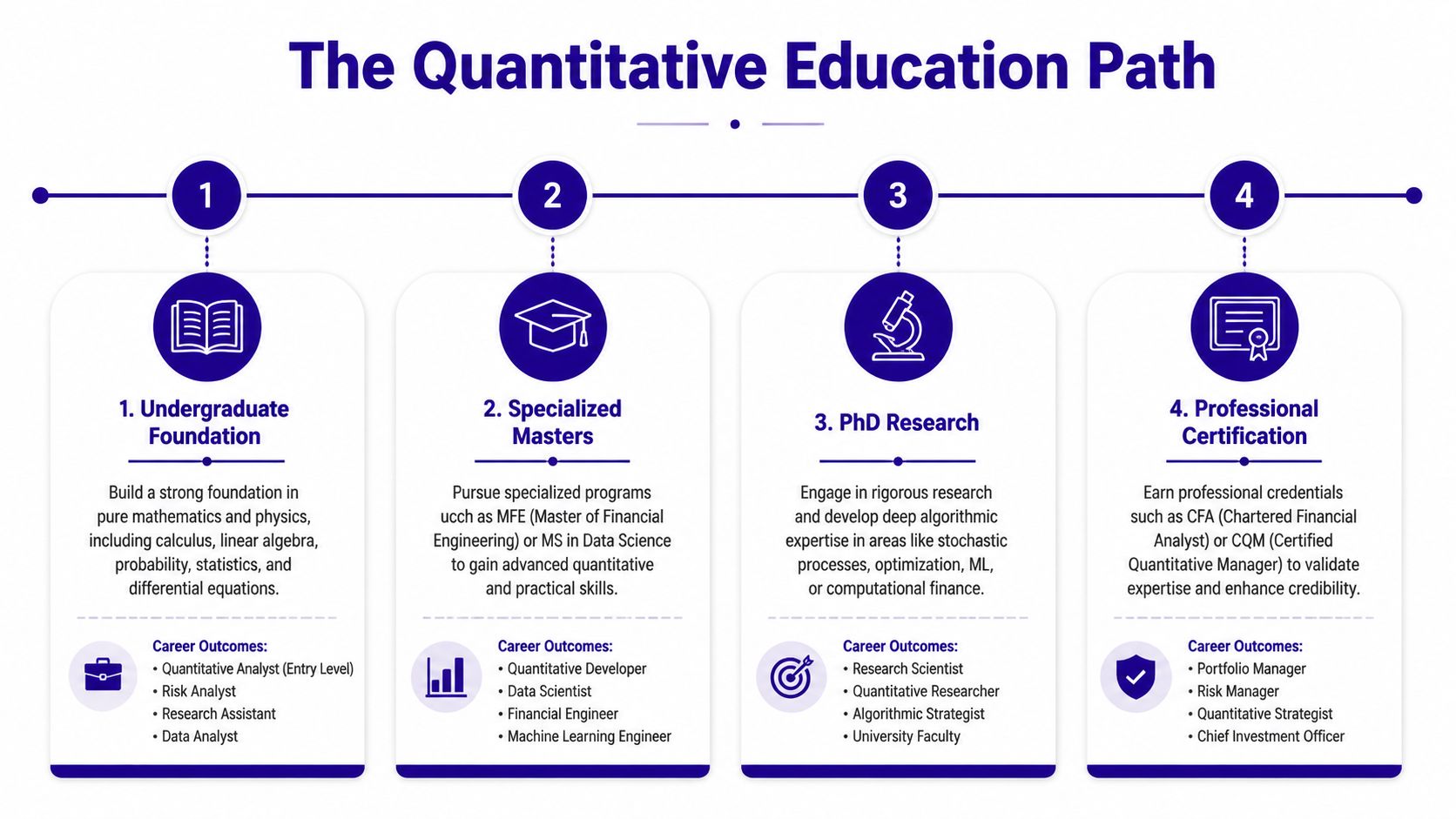

Building Your Academic and Mathematical Foundation

The most direct route into elite quant roles is still the academic route. A PhD in a quantitative discipline remains the gold standard, with approximately 80 to 90% of researchers at top hedge funds and proprietary trading firms holding doctoral degrees in fields like Physics, Mathematics, or Computer Science, according to QuantStart’s guide to becoming a quantitative analyst.

That doesn’t mean every candidate needs a doctorate. It does mean candidates should understand what the PhD signals to employers. It signals independence, deep problem solving, comfort with abstraction, and the ability to push through open-ended research without supervision.

Choosing the right degree path

A bachelor’s degree can be enough for some entry points, but it usually needs to be in a rigorous field and paired with unusually strong projects, internships, or competition performance. Mathematics, physics, computer science, statistics, and engineering remain the strongest foundations.

A master’s degree is the middle path. It can work well for candidates who already have a technical undergraduate degree and want tighter alignment with finance, machine learning, or computational methods. Programs in financial engineering, computational finance, statistics, applied math, and data science can all be relevant if the coursework is hard enough and the student uses the program to build a real hiring profile.

A PhD is different. It is still the best route for research-heavy roles at the most selective firms. That’s especially true when the role involves alpha research, statistical modeling, optimization, or machine learning research. The degree itself doesn’t guarantee anything. The true asset is what the training proves.

A strong degree doesn’t rescue a weak candidate. It simply gives a strong candidate the cleanest path into the hardest rooms.

Candidates planning their education should think less about prestige in the abstract and more about signal density. The best program is the one that forces hard mathematics, demands coding, and gives access to projects or internships that can survive technical scrutiny.

For candidates mapping long-term progression, this data science career path guide is useful because it frames how technical depth compounds into specialized roles over time.

What to study if the background is not technical

Many guides fail at this point. They assume the candidate already knows linear algebra, probability, and programming.

Some don’t. That doesn’t make the path impossible. It makes the path slower and less forgiving. Verified background data indicates that 15 to 20% of quant hires at top firms come from non-traditional paths, often through bootcamps or specialized training, as noted in this QuantStart-linked discussion of non-traditional quant entry. The key phrase is not “non-traditional.” It’s “can demonstrate the required skills.”

For a non-technical candidate, the right order matters more than speed:

-

Start with linear algebra and calculus

Matrices, eigenvalues, optimization basics, derivatives, integrals, and multivariable thinking show up everywhere. -

Then build probability and statistics

Random variables, conditional probability, expectation, variance, distributions, estimation, hypothesis testing, regression, and time series are core. -

Only then push into finance-specific math

Stochastic calculus, derivatives pricing, Monte Carlo methods, and numerical methods make sense once the base is real. -

Learn programming in parallel, not later

Python first. Then C++ if targeting low-latency, infrastructure-heavy, or developer roles.

A weak foundation creates a predictable failure mode. Candidates jump into options pricing or machine learning because those topics feel advanced. Then interviews expose missing basics in probability, algebra, or coding.

The math that actually matters

The market doesn’t care whether a candidate has seen an advanced topic once. It cares whether the candidate can use it.

The most valuable subjects are:

- Probability and statistics

- Linear algebra

- Calculus and optimization

- Time series analysis

- Numerical methods

- Stochastic processes

- Machine learning, used carefully

Candidates should aim to implement what they study. If a topic can’t be coded, tested, and explained, it probably isn’t interview-ready yet.

Mastering the Quant Technical Stack

According to Carnegie Mellon’s overview of quant preparation, 95% of job requirements mandate proficiency in probability and statistics plus languages like Python and C++, and those skills are used in 90% of quant roles for derivatives pricing, market microstructure analysis, and arbitrage strategies in this CMU quant career guide.

That hiring pattern should shape how candidates train. Instead of collecting languages, focus on knowing which tool solves which class of problem and proving you can use it under interview pressure.

Why Python and C++ serve different jobs

Python is the research language in a large share of quant teams because it speeds up iteration. It is well suited to signal research, exploratory analysis, factor testing, feature engineering, and model evaluation. Pandas, NumPy, and scikit-learn matter because they let candidates test ideas quickly and spend more time judging results than wiring basic infrastructure.

C++ matters when performance is part of the job description. Firms use it for execution systems, market data handlers, exchange connectivity, simulation engines, and infrastructure where latency and memory behavior matter. Candidates targeting quant developer roles, electronic trading, or HFT should expect stronger scrutiny on C++, systems knowledge, and code quality than pure researchers usually face.

SQL gets screened less often in branding-heavy advice, but it shows up constantly on the job. Real research work involves messy joins, stale fields, broken timestamps, corporate actions, and vendor inconsistencies. A candidate who can query and validate data cleanly saves a team time. A candidate who cannot usually creates hidden errors that show up later in bad signals and failed models.

Candidates who need to fill gaps in data workflows, model implementation, or ML tooling can use this roundup of machine learning and data science websites as a practical supplement.

Essential Quant Technical Skills

| Skill/Tool | Primary Application | Required Proficiency |

|---|---|---|

| Python | Research, backtesting, data analysis, prototyping | Strong enough to build clean end-to-end projects |

| C++ | Low-latency systems, execution, high-performance infrastructure | Strong for developer and HFT-oriented roles |

| SQL | Querying, joining, validating large datasets | Comfortable with production-style data work |

| Pandas and NumPy | Data wrangling, vectorized analysis, numerical workflows | Daily-use level |

| scikit-learn | Baseline ML workflows and model evaluation | Practical, not buzzword-level |

| Probability and statistics | Model design, inference, testing, interview problem solving | Deep conceptual command |

| Time series analysis | Forecasting, signal construction, regime analysis | Able to implement and critique |

| Monte Carlo and numerical methods | Pricing, simulation, stress-testing | Working implementation ability |

| Bloomberg Terminal or similar data tools | Historical data access and market context | Functional familiarity |

What works and what doesn’t

Two failure modes show up again and again in quant hiring. One group studies theory for too long and cannot build anything usable. Another group learns libraries and APIs fast but cannot explain the assumptions, edge cases, or failure points in their own models.

The strongest candidates pair concepts with implementation and then push one step further. They test data quality before modeling. They check whether results survive transaction costs, regime changes, and parameter sensitivity. They profile code when speed matters. They can explain why a backtest looked good, why it broke, and what they changed.

The candidate who can explain why a model fails is usually stronger than the candidate who can only show when it worked.

This is also where recruiting reality matters. Hiring managers rarely read every line of a resume or GitHub repository. Recruiters who specialize in quant can help position the right technical evidence for the right desk, especially when the difference between research, trading, and quant dev roles is not obvious from the outside. On the resume itself, stop listing tasks, show your results. A hiring team wants to see what you built, how you tested it, what constraints you handled, and what improved because of your work.

Technical maturity is visible fast. Teams can tell whether a candidate has worked with noisy data, debugged edge cases, and made sensible trade-offs between speed, accuracy, and maintainability. That is the standard the stack needs to support.

Creating a Portfolio That Gets You Noticed

A serious quant portfolio doesn’t need to be large. It needs to be convincing.

That means fewer projects, done properly. The standard isn’t whether a notebook runs. The standard is whether the work shows research discipline, implementation ability, and judgment about what makes a result believable. QuantStart’s self-study guidance is useful here because it stresses that professional-grade work includes implementing models programmatically, testing across multiple training and testing splits, and using the deflated Sharpe ratio to reduce data-snooping errors in this self-study plan for becoming a quantitative trader.

Three projects that signal real ability

The first strong project is a simple event-driven backtester. It doesn’t need to look like institutional infrastructure, but it should handle positions, signals, transaction assumptions, and portfolio state cleanly. This shows engineering discipline. It also forces the candidate to think about design, not just model output.

The second is a statistical strategy project, such as pairs trading, mean reversion, or cross-sectional ranking. Many candidates expose weak reasoning during this phase. A good version shows data cleaning, feature construction, proper train-test separation, and skepticism about attractive results.

The third is a pricing or simulation project. Monte Carlo option pricing, finite-difference approximations, or numerical experiments around volatility models work well because they expose mathematical fluency and implementation accuracy.

Professional-looking projects don’t impress by being flashy. They impress by closing obvious loopholes before an interviewer has to point them out.

How to present the work

A project only helps if it can survive resume review in under a minute.

Each project should include:

- A clear problem statement: What was tested or built.

- Method choice: Why that approach made sense.

- Data notes: What was used, cleaned, or excluded.

- Validation method: How leakage and overfitting were addressed.

- Result interpretation: What the candidate believes and what remains uncertain.

- Code quality: Readable structure, modular functions, basic documentation.

Resume bullets matter here. Generic task descriptions bury good work. Candidates get better outcomes when they follow the principle to stop listing tasks, show your results, especially when describing projects that combine math, engineering, and market logic.

A portfolio should also avoid common mistakes:

- Don’t upload only notebooks. Include reusable modules and a short README.

- Don’t hide failed tests. Briefly documenting what didn’t hold up shows maturity.

- Don’t present toy finance as quant research. A moving-average crossover with no rigor won’t help.

- Don’t overclaim. If the method is exploratory, say so.

One excellent project is worth more than five shallow ones. Hiring managers and recruiters both know the difference quickly.

Navigating the Quant Job Hunt and Interview Gauntlet

Top quant seats often hire a tiny fraction of applicants, and that reality shapes the whole search. Good candidates miss interviews, fail loops, or get screened out long before anyone tests their ceiling. The problem is usually fit, signaling, and process discipline.

Quant hiring is harder to read from the outside than software or general finance hiring. The same title can point to alpha research, pricing, execution, low-latency engineering, model validation, or data-heavy infrastructure work. A candidate who applies with one generic resume and one generic story usually burns time.

What a quant resume needs to show fast

Resume review is brutally short. In many teams, the first pass is a fast scan for evidence that the candidate can survive a technical screen and belongs in that specific seat.

A quant resume should surface the right signals early:

- Academic signal: Degree, coursework, thesis, research area

- Technical stack: Python, C++, SQL, numerical tools, ML libraries

- Project proof: Backtesting, simulation, pricing, forecasting, market data work

- Evidence of rigor: Publications, olympiads, Kaggle only if relevant, serious open-source work

- Role fit: Research-heavy resumes should look different from developer-heavy resumes

The ordering matters. If a candidate is strong in stochastic processes, optimization, market microstructure, or systems work, that should not be buried under generic leadership bullets. Hiring managers are trying to answer a narrow question fast. Can this person do this job?

Candidates targeting prop firms should also read job language carefully across firms before applying. MyFundedCapital is a useful reference point for how proprietary trading roles are framed and how those postings differ from hedge fund and bank roles. That comparison helps candidates avoid applying to execution-heavy or discretionary seats when their background points to research or engineering.

How interviews break candidates

Interview failure points are predictable. The breakdown is often translation, not raw intelligence. Strong students struggle when they have to think aloud under pressure, write clean code without an IDE, or adapt when an interviewer changes one assumption in a familiar problem.

Preparation needs multiple tracks running at once:

-

Probability and statistics

Conditional probability, expectation, distributions, estimation, testing, and reasoning under uncertainty. -

Mental math

Fast arithmetic, approximations, sanity checks, and staying composed without a calculator. -

Coding

Data structures, algorithms, implementation quality, runtime trade-offs, and edge cases. -

Role-specific depth

Researchers need stronger modeling judgment. Developers need stronger systems thinking and C++. Traders need stronger market intuition and faster decision quality.

The common mistake is narrow prep. Candidates drill classic brainteasers or memorize solutions from popular interview books, then stall as soon as the problem is modified. As noted earlier, acceptance rates are low and patterned memorization fails once interviewers push one layer deeper.

One sentence usually reveals the gap. A candidate can state the formula, but cannot explain the assumptions, failure modes, or why a different approach might be better under time pressure.

Quant interviews reward clear reasoning under variation. They punish brittle preparation.

Where specialized recruiters add real value

Specialized recruiters have real value in quant because the market is opaque and firm-specific. A good recruiter knows which teams care about Olympiad pedigree, which groups will trade that off for production experience, and which interviews are dominated by probability, C++, market intuition, or research discussion.

That matters more than candidates expect. I have seen strong applicants waste months targeting firms that were structurally wrong for their profile. A master’s candidate with sharp coding and decent market instincts should be positioned differently from a PhD with published research and weaker implementation speed. Sending both through the same process story lowers response rates.

The best recruiters help in four concrete ways:

- Calibration: Which firms and teams fit the candidate’s current profile

- Positioning: How to frame strengths without overselling weak spots

- Process management: How to sequence applications and keep parallel interview loops active

- Debriefing: How to turn vague feedback into a better next-round plan

There is a trade-off here. Weak recruiters spray resumes and add noise. Strong recruiters improve targeting, preserve optionality, and give candidates context they would struggle to get on their own. In quant, that context often changes outcomes.

Networking still matters, but generic outreach rarely works well. Specific outreach does. A short note about a paper, strategy area, project, or open role gets better responses than broad requests for advice. That is how serious candidates get into the right conversations.

Your First Year as a Quant and Beyond

A large share of new quant hires struggle for a simple reason. The job changes once your work touches real positions, real risk limits, and production systems.

Getting the offer is only the start. The first year is where teams decide whether you are a strong long-term hire, a narrow specialist, or someone who interviewed better than they execute. That judgment is usually made on small pieces of work before it is made on big ones.

What the first year feels like

Expect compression. You are learning the codebase, the data lineage, the research process, the deployment rules, and the firm’s internal standard for evidence at the same time. The technical gap is real, but the bigger adjustment is operational discipline. Good ideas are cheap if they cannot be reproduced, reviewed, and shipped safely.

Early tasks often look less glamorous than candidates expect. Cleaning messy data. Checking whether a signal survived a change in methodology. Reproducing an old result from scratch. Reading internal libraries before writing anything new.

That work is the audition.

Teams use it to answer practical questions. Can this person debug without creating noise? Can they tell the difference between a data issue and a model issue? Can they write research that another quant can follow six months later? Pedigree matters far less once those questions are live.

The fastest way to lose trust is also predictable. Overstated backtests, undocumented assumptions, and code that works once on a laptop but fails in the team’s environment will get noticed quickly.

What separates people who stay from people who stall

The first separator is reliability. Senior quants remember the new hire who can take an ambiguous task, clarify the objective, and return with clean results and sensible caveats. They also remember the one who needs constant rescue.

The second is taste. Strong early-career quants learn what matters on their desk. On one team that may mean execution quality and latency discipline. On another it may mean careful experimental design, cleaner inference, or better communication with PMs and engineers. Smart people stall when they optimize for the wrong metric.

The third is question quality. Good juniors do not ask for a walkthrough of everything. They do the first pass themselves, isolate the confusing part, and ask a question that moves the work forward. That behavior signals judgment, not just curiosity.

Career progression after year one usually follows one of three paths. Some quants become trusted implementers who are excellent at turning research into production. Some become researchers with increasing ownership over alpha ideas, model design, or portfolio construction. Others move toward hybrid roles that require commercial judgment, team coordination, and enough technical depth to challenge weak assumptions.

This is also the point where outside market context starts to matter again. A specialized recruiter can tell you whether your first seat is building the right career capital or trapping you in a narrow story that will be hard to sell later. Two years of strong work on the wrong desk can still make your next move harder than one good year on a team with better training, cleaner ownership, and clearer PnL relevance. Candidates often miss that trade-off when they focus only on title or compensation.

Long careers in quant finance are built on a simple pattern. Learn the desk’s standards fast. Produce work other people can trust. Keep compounding skill after the novelty of the offer wears off.

Candidates who are serious about breaking into quant finance, or moving from a good technical role into a better-aligned one, should get expert help early. nexus IT group works with specialized technology and quant hiring markets, and that kind of focused guidance can make the difference between sending applications into a black hole and getting in front of teams that match the profile.