Candidates who get quant offers usually do two things well under pressure. They solve the problem, and they show they understand why that problem matters for the role.

That distinction decides interviews more often than candidates expect. A quant research screen can test statistical judgment, model risk, and experimental design. A trading interview can reward speed, estimation, and market intuition. A quant developer loop often puts more weight on implementation quality, edge cases, and performance constraints. The same probability question can be used in all three settings, but the bar for a strong answer changes with the seat.

Good preparation reflects that reality. Generic lists of quant interview questions help with coverage, but they rarely explain what the interviewer is actually scoring. That is the gap this guide addresses. Each question is grouped by topic and tied to the role context behind it, so candidates can see the technical solution, the hidden evaluation criteria, and the mistakes that make an otherwise capable applicant hard to place.

From a staffing perspective, placeable candidates are rarely the ones with the flashiest answer. Firms remember candidates who structure ambiguity well, state assumptions clearly, catch practical pitfalls, and adjust depth to the interviewer. That same pattern shows up in adjacent technical hiring too, including data science interview preparation strategies, where employers screen for reasoning quality, not just final output.

The goal is to prepare at that level. Not by collecting tricks, but by learning how probability, market microstructure, statistics, stochastic calculus, optimization, machine learning, coding, and behavioral judgment are tested in actual quant interviews.

Table of Contents

- 1. Probability & Statistics Coin Flip Expected Value Problem

- 2. Market Microstructure The Bid-Ask Spread Arbitrage Question

- 3. Statistics & Hypothesis Testing Multiple Comparisons Problem

- 4. Stochastic Calculus Black-Scholes Option Pricing Derivation

- 5. Optimization & Algorithm Design Portfolio Optimization Problem

- 6. Machine Learning & Prediction Model Overfitting & Cross-Validation

- 7. Coding & Implementation Efficient Algorithm Design Median Finding Sorting Problem

- 8. Behavioral & Domain Knowledge Trading Loss Scenario Management

- Quant Interview Questions: 8-Topic Comparison

- Beyond the Questions Your Path to a Quant Offer

1. Probability & Statistics Coin Flip Expected Value Problem

Small probability puzzles carry a lot of weight in quant hiring because they reveal process fast. A coin-flip expected value question can tell an interviewer, in under five minutes, whether a candidate defines assumptions cleanly, chooses an efficient method, and distinguishes payoff from risk.

A standard version is simple to state. Flip a fair coin until the first tail. Each head pays a fixed amount. Find the expected value of the game.

The math is usually manageable. The key test is whether the candidate structures the answer like someone who can work on a desk, in research, or in a production-facing quant role.

What the interviewer is really checking

Interviewers are usually scoring four things at once.

First, model setup. Strong candidates state the stopping rule, confirm independence, define the payoff per head, and make the terminal condition explicit before writing equations.

Second, method choice. In an interview, recursion is often the best route because it is short and easy to audit. Infinite-series expansion also works, but only if the candidate can keep the notation controlled.

Third, judgment. A placeable candidate does not treat expected value as the whole story. They mention distribution shape, tail behavior, and whether the result would still matter if the variance were large relative to the mean.

Fourth, communication under pressure. Staffing teams and hiring managers both notice this. A candidate who can explain the setup in plain language is easier to trust with PMs, traders, and engineering partners than someone who reaches the right answer through opaque algebra.

Candidates targeting hybrid quant and data-heavy roles often sharpen this skill set through broader data science interview preparation, especially around variable definition, assumptions, and verbal reasoning.

A strong answer, step by step

Start by naming the random structure. Let (E) be the expected value of the game. On the first flip, there are two cases.

With probability (1/2), the coin lands tail and the game ends immediately with zero additional payoff. With probability (1/2), the coin lands head, the candidate earns the fixed payout, and the game resets into the same expected value problem.

That gives the recursive equation:

[

E = frac{1}{2}(0) + frac{1}{2}(p + E)

]

Solve it cleanly:

[

E = frac{p + E}{2}

]

[

2E = p + E

]

[

E = p

]

If each head pays $1, the expected value is $1.

This is the kind of result that catches candidates who rush. The answer feels smaller than some expect because long streaks are possible, but they are weighted by rapidly shrinking probability.

What separates a pass from a strong pass

A pass gets the recursion right.

A strong pass adds interpretation. The candidate says the expected number of heads before the first tail is 1, so the result is consistent with intuition. They also note that expected value is not the same as typical realized outcome. Many paths end quickly. A few longer runs contribute disproportionately to the mean.

That distinction matters by role. For a quant researcher, it shows statistical maturity. For a trader or market maker, it signals awareness that attractive expectation can still come with unstable pathwise outcomes. For a recruiter or staffing partner assessing placeability, it signals the candidate can move beyond puzzle mechanics and discuss why the result matters in practice.

One more point helps. If time permits, show the series form:

[

E = sum_{k=1}^{infty} k p cdot Pr(text{exactly } k text{ heads before first tail})

]

or describe that each additional head contributes less because the probability halves each round. The point is not to show off. The point is to confirm the answer from a second angle.

Candidates who want a plain-language market refresher alongside these probability drills often also benefit from bid-ask spread explained, since many interviews mix math puzzles with trading mechanics.

Common mistakes

Candidates lose points when they:

- write equations before defining the game state

- confuse expected payout with the most likely outcome

- ignore whether the payout is fixed per head or changes by round

- keep pushing algebra after reaching the result instead of interpreting it

In practice, interviewers remember the candidate who is organized, checks the answer against intuition, and explains the trade-off between clean expectation and noisy realized paths. As noted earlier, firms hiring for quant research care about much more than puzzle speed. They want evidence that the candidate can reason clearly, defend assumptions, and connect math to decision-making.

2. Market Microstructure The Bid-Ask Spread Arbitrage Question

This question tends to expose whether someone understands markets or has only studied textbook pricing. A stock shows a bid and an ask. The interviewer gives tradable prices and asks how value could be captured. Many candidates say “buy at the bid and sell at the ask,” which immediately signals that they haven't internalized who can trade where.

That mistake matters more in market making and systematic trading interviews than in pure research loops. The desk wants someone who understands queue position, inventory, fill uncertainty, and the difference between a quoted spread and an earned spread.

Where candidates go wrong

The bad answer assumes frictionless arbitrage. Real markets rarely offer free money at displayed prices, especially once latency, adverse selection, and partial fills enter the conversation. A more thoughtful answer starts by saying that if both prices are instantly executable, the first question is whether the setup is realistic.

Then the candidate reframes. A market maker doesn't “take” both sides at once. A market maker posts liquidity, gets hit or lifted selectively, manages inventory, and tries to earn spread net of losses from informed flow.

For candidates who need a concise refresher on the trading mechanics behind this, bid-ask spread explained is a useful plain-language reference.

What a placeable answer sounds like

From a staffing perspective, the candidates who move forward usually sound operational. They ask what venue is involved, whether the prices are stale, whether the trader can post or only cross, what the position limits are, and what happens if only one side fills.

A strong microstructure answer sounds less like a classroom proof and more like a pre-trade checklist.

Useful points to include:

- Execution assumptions: Can orders rest, or must they cross the spread?

- Inventory management: Spread capture can turn into directional risk quickly.

- Latency sensitivity: A stale quote can disappear before the order reaches the book.

- Hedging logic: If the trade is part of a relative-value setup, what offsets the exposure?

What doesn't impress interviewers is fake certainty. Saying “this is an arbitrage” without probing the mechanics usually ends the conversation in the wrong direction.

3. Statistics & Hypothesis Testing Multiple Comparisons Problem

A lot of quant candidates can define a p-value. Fewer can explain why a research process with enough trials will almost always produce a few apparently strong results by accident. That is the core of this question.

Interviewers ask it because false positives are expensive. A desk can spend months allocating capital, engineering time, and credibility to a signal that was only the best survivor from a crowded test set. From a staffing perspective, this is also a placeability filter. Firms want candidates who can protect a research pipeline, not just generate more ideas for it.

What the interviewer is really assessing

The surface question is statistical. The underlying test is judgment.

A strong candidate identifies the setup quickly. If dozens or hundreds of factors, entry rules, horizons, or parameter combinations were tested, standard significance thresholds stop meaning what they appear to mean in isolation. One result with a low p-value is weak evidence when it comes from a large search process.

The better answers also separate roles. For a quant researcher, the expected response is methodological control. For a trader or PM-facing quant, the expected response includes business consequences. How much capital would be put behind the finding, how unstable is the edge, and what happens after costs and regime shifts are introduced?

A solid answer structure

A credible response usually covers four points:

- State the problem clearly: multiple testing increases the chance of false discoveries.

- Choose an adjustment: Bonferroni is stricter and reduces false positives, while false discovery rate methods are often more practical in exploratory research.

- Protect validation: keep discovery and confirmation separate with a true out-of-sample test, not a recycled holdout that has already influenced decisions.

- Check economic logic: a statistically significant signal with no plausible mechanism is often a data-mined artifact.

That trade-off matters. Bonferroni can be too conservative if the firm is screening a large feature library and can tolerate some false leads early. FDR control is often a better fit for research environments that expect many candidates to fail later under stricter validation. Interviewers notice when candidates can explain that choice instead of reciting correction names from memory.

Pitfalls that weaken an otherwise good answer

Candidates lose points when they stop at “apply a correction.” In practice, multiple comparisons problems usually arrive bundled with other research mistakes: feature mining, leakage across train and test periods, repeated reuse of the same holdout set, and parameter tuning that keeps going until the Sharpe ratio looks presentable.

Placeable candidates sound careful with process. They ask how many hypotheses were tried, whether tests were pre-specified, whether features were selected using future information, and whether the signal still works after turnover, slippage, and market impact are modeled. For a trading strategy, statistical significance alone is not enough. Execution can erase the edge. For a quick refresher on that friction, the bid-ask spread explained is a useful practical reference.

What firms trust is controlled skepticism. The candidate should protect against false discovery without shutting down useful research.

The strongest answers sound like someone who has worked with noisy alpha generation. They know that the goal is not to eliminate every false positive at the first stage. The goal is to design a process that lets weak signals die cheaply and lets stronger ones face progressively harder tests before capital is committed.

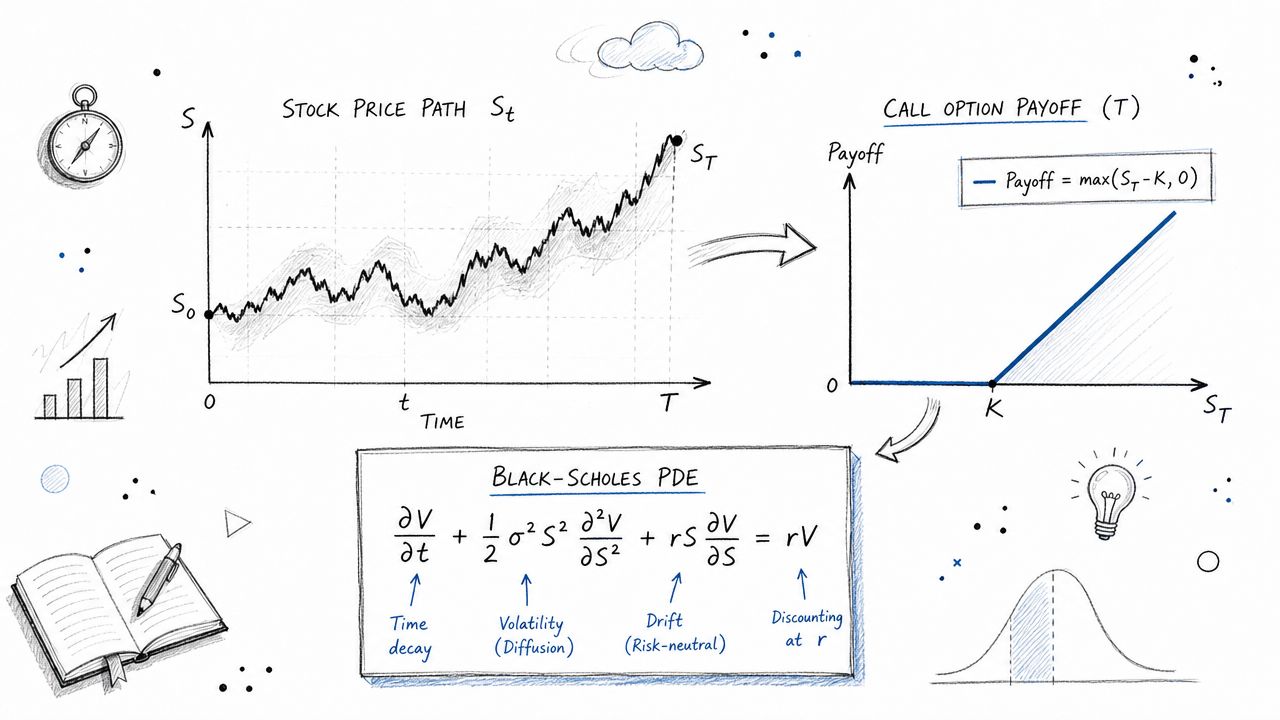

4. Stochastic Calculus Black-Scholes Option Pricing Derivation

At this point, interviews stop feeling broad and start feeling selective. If a firm asks for a Black-Scholes derivation, it isn't checking whether the candidate has seen the formula before. It's checking whether the candidate can move from assumptions to dynamics to pricing logic without losing the thread.

Some candidates make the mistake of trying to impress with notation density. That usually backfires. Interviewers generally prefer a clean derivation with clear economic interpretation over a rushed wall of symbols.

What separates a pass from a strong pass

A pass-level answer usually states the stock process, applies Itô's lemma to the option value, constructs the hedged portfolio, removes the diffusion term, and arrives at the pricing PDE.

A stronger answer goes further. It states the assumptions explicitly, such as frictionless markets, continuous trading, no arbitrage, and constant volatility. It also explains why those assumptions matter and where they break in practice.

What interviewers notice: Candidates who can explain the hedge intuition while deriving the PDE usually perform better than candidates who only recite the derivation mechanically.

How to present the derivation under pressure

A disciplined structure helps:

- Start with dynamics: Write the stock process clearly.

- Apply Itô's lemma carefully: Most errors happen here.

- Construct the hedge: Show how the stochastic term is neutralized.

- Connect to pricing: A riskless portfolio must earn the risk-free rate under the model assumptions.

- State limitations: Volatility smile, jumps, discrete hedging, and transaction costs all limit the model in practice.

That last step matters. Quant interview questions at this level often reward candidates who can move between theory and implementation. A candidate who knows the formula but can't discuss model risk usually looks less useful than one who can connect the PDE to practical pricing and hedging limits.

5. Optimization & Algorithm Design Portfolio Optimization Problem

Portfolio optimization questions are less about elegant matrix notation than many candidates expect. The interviewer already knows the textbook setup. The core question is whether the candidate understands why the textbook setup often fails in production.

A minimum-variance portfolio with long-only and position-cap constraints sounds straightforward. In practice, the result can be dominated by estimation error, unstable covariance inputs, and awkward constraint interactions.

What employers actually care about

A good answer names the optimization class and the likely toolchain. For many candidates, that means framing the problem as a convex quadratic program and mentioning implementation options like cvxpy or a commercial solver.

A better answer immediately adds practical skepticism. Covariance estimates are noisy. Small input changes can produce very different weights. Long-only and max-weight constraints may improve realism, but they don't magically fix bad estimates.

A practical response structure

The most convincing responses usually follow this sequence:

- Formulate the objective: Minimize portfolio variance subject to weight constraints.

- Specify constraints clearly: Sum of weights, long-only bounds, and position caps.

- Address estimation risk: Shrinkage, regularization, or stable optimization may be needed.

- Discuss validation: Walk-forward testing matters more than a single in-sample optimum.

- Handle implementation: Rebalancing frequency and turnover constraints affect whether the solution is usable.

Candidates who stop at “solve the matrix problem” often miss the hiring signal. Firms want evidence that the person can build portfolios that survive contact with noisy data and operational limits.

This is also where role differences become obvious. A researcher may be expected to discuss statistical estimation and regime instability. A quant developer may be pushed harder on solver behavior, runtime, and numerical stability. A placeable candidate can shift depth depending on which seat is being filled.

6. Machine Learning & Prediction Model Overfitting & Cross-Validation

A surprising share of weak quant interview answers still treat overfitting as a tuning problem. In practice, interviewers often use this question to test whether a candidate can distinguish a bad model from a bad experiment.

That distinction matters in finance more than in generic ML settings. Time order matters. Feature timestamps matter. Label construction matters. A model can look excellent because the pipeline leaked future information or because the validation split ignored serial dependence.

Interviewers are usually assessing three things at once. First, does the candidate understand what can go wrong in financial data. Second, can they set up an evaluation process that would survive scrutiny on a real desk. Third, can they explain trade-offs by role. A research candidate should talk about regime instability, target design, and whether the signal survives transaction costs. A quant developer may get pushed harder on reproducible pipelines, split logic, and how to prevent preprocessing mistakes in production.

The strongest answers start with the experiment, not the model. They ask practical questions. Were features timestamped at the moment they were observable? Was scaling fit only on the training window? Did overlapping samples create hidden leakage? Was random k-fold used on time-series data where walk-forward testing was the right choice?

A disciplined response usually covers these points:

- Audit leakage first: Check timestamps, joins, normalization, target horizon, and any feature built with revised or delayed data.

- Choose time-aware validation: Use expanding-window or rolling-window splits for ordered market data instead of random shuffles.

- Control complexity after the setup is valid: Regularization, feature selection, and simpler models help, but only after the evaluation design is credible.

- Separate model selection from final testing: Cross-validation chooses the model. A clean holdout tests whether the process generalizes.

- Explain instability clearly: A drop from train to test performance may reflect regime change, weak signal, or target noise, not just excessive model capacity.

Candidates often miss one hiring signal here. Firms are not only asking, "Can this person name the right techniques?" They are asking, "Would I trust this person to avoid shipping a misleading backtest?" From a staffing perspective, that directly affects placeability. Candidates who can explain both the math and the failure modes are easier to put in front of hiring managers because they sound closer to someone who has worked with live model risk.

For interviews conducted in a shared editor or whiteboard setting, it also helps to practice explaining validation logic clearly under time pressure. This kind of virtual whiteboard interview preparation for coding and model explanation is useful because interviewers care about structure as much as terminology.

If you want a concise refresher on algorithmic thinking behind train-test procedures and data handling, this Maeve learning resource is a reasonable supplement.

One final pitfall. Candidates often jump to "I would use cross-validation" and stop there. A better answer specifies which cross-validation scheme fits financial data, what it protects against, and what it still does not solve. That level of precision is usually what separates a candidate who has studied machine learning from one who can be trusted to build predictive systems in a quant role.

7. Coding & Implementation Efficient Algorithm Design Median Finding Sorting Problem

Some quant candidates still underestimate coding rounds. That's a mistake. Even research-heavy teams increasingly care whether the candidate can turn a clean idea into clean code without falling apart on edge cases.

Median-of-two-sorted-arrays is a good example because it reveals both algorithmic maturity and communication. The brute-force merge is easy to explain. The logarithmic partition-based method is what usually separates good from excellent.

How strong candidates structure the coding answer

The strongest approach isn't to jump straight to the optimal solution. It's to show progression. Start with the obvious merge-based idea, explain its time and space trade-offs, then improve it by partitioning the smaller array and checking the boundary conditions.

That progression matters in virtual interviews. A candidate who narrates trade-offs and keeps the whiteboard or shared editor organized is easier to trust in team settings. For that environment, virtual whiteboard coding interview preparation is directly relevant.

What interviewers remember

Interviewers usually remember these signals more than the final syntax:

- Choice of search space: Binary search should run on the smaller array when sizes differ significantly.

- Boundary handling: Empty arrays, duplicate values, and odd versus even total length should be addressed explicitly.

- Complexity explanation: Strong candidates explain why the optimized method improves on the brute-force baseline.

- Code clarity: Variable names, branch logic, and tests all matter.

A supplemental reference on algorithm and data-structure fundamentals is this Maeve learning resource, though interview performance still depends far more on deliberate practice than on passive review.

Candidates often lose points by solving the problem without explanation. In quant interview questions, especially hybrid coding screens, explanation is part of the score.

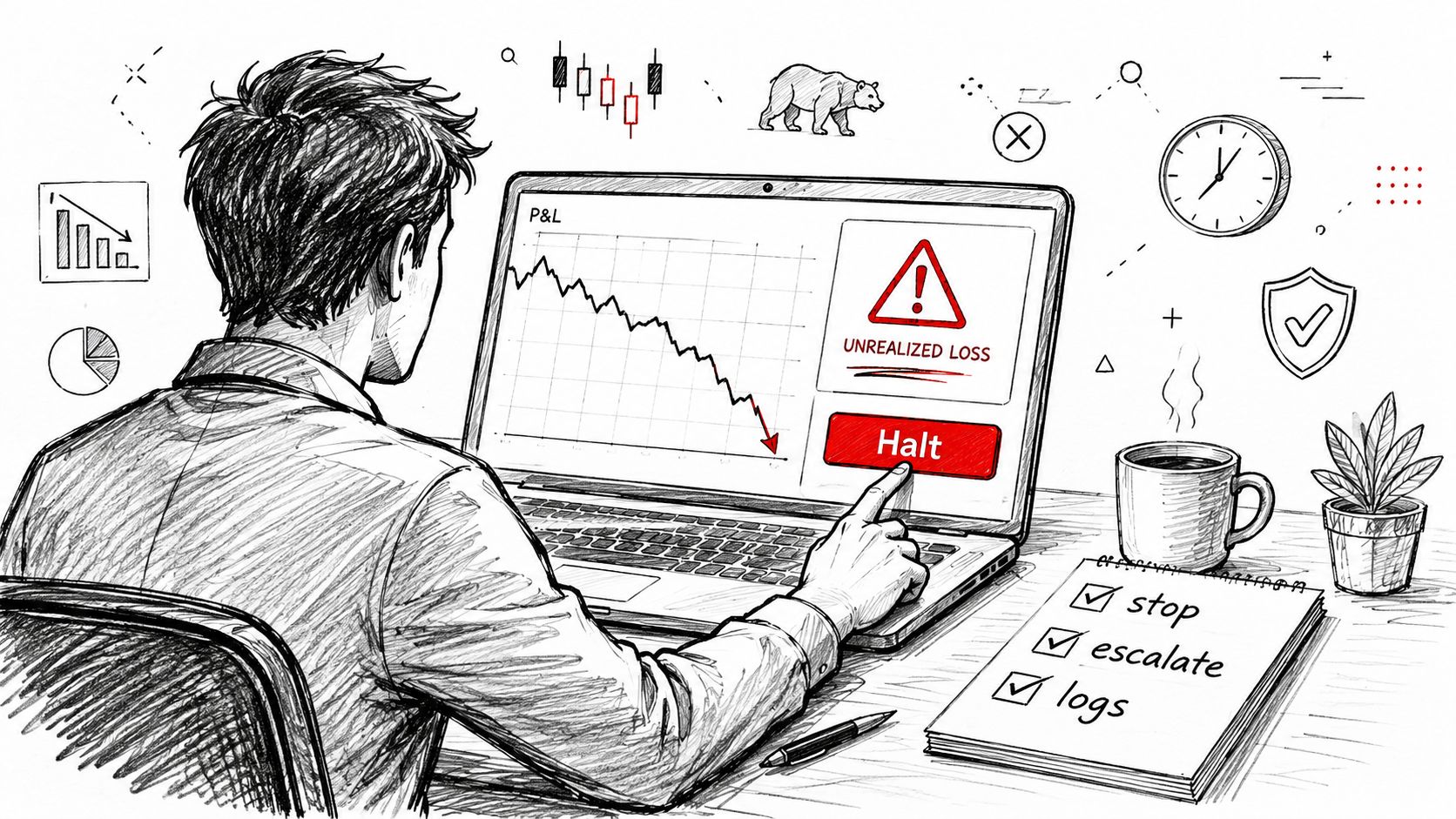

8. Behavioral & Domain Knowledge Trading Loss Scenario Management

A trading-loss prompt separates candidates who can solve models from candidates a desk can trust with risk. Interviewers use it to test judgment under pressure, because a bad first response in production can turn a manageable loss into a control failure.

The setup is usually simple on purpose. A low-risk strategy starts losing money fast. The interviewer is not asking for a brilliant market call. They want to see whether you protect capital, respect limits, and communicate clearly before chasing an explanation.

The common failure mode is thesis attachment. Candidates start defending the trade, waiting for mean reversion, or arguing that the model is usually right. On a real desk, that answer raises concerns about placeability. Hiring managers and staffing teams both know that firms can train product detail faster than they can fix weak escalation habits.

A stronger answer follows an operational sequence:

- Contain exposure: Reduce or stop trading if your controls and authority allow it.

- Confirm the loss path: Check whether PnL is driven by market movement, bad market data, stale positions, hedge slippage, or execution issues.

- Escalate early: Bring in risk, the desk lead, and engineering or support teams before the situation gets harder to reconstruct.

- Preserve evidence: Save logs, orders, timestamps, model inputs, and state snapshots.

- Fix the control gap: Add limits, alerts, monitoring, or kill-switch logic based on the failure point.

Interviewers are usually assessing three things at once. First, do you understand that risk management outranks intellectual pride. Second, can you distinguish market risk from system risk. Third, can you communicate in a way that helps a team act quickly.

Good candidates also name the trade-offs. Halting a strategy too fast can interrupt legitimate positions and give up edge. Waiting too long can multiply losses and create governance problems. The right answer shows you know the cost of both errors, but still choose controlled action over improvisation.

A concise response can sound like this: contain the risk, verify whether the loss is real, identify whether the problem is market, model, data, or execution, escalate with specific facts, then document the post-mortem and tighten controls. That answer signals maturity.

This topic also reveals whether a candidate understands the job beyond textbook math. Candidates who want a clearer view of how trading judgment, technical depth, and communication fit together can review this guide on how to become a quant.

Quant Interview Questions: 8-Topic Comparison

| Topic | Assessment focus | Implementation complexity | Resource requirements | Expected outcomes | Ideal use cases |

|---|---|---|---|---|---|

| Probability & Statistics: Coin Flip Expected Value Problem | Recursive reasoning, expected value, infinite series | Low, short analytical derivation | Minimal, pencil/whiteboard; basic math | Reveals mathematical rigor and comfort with expectation/variance | Entry/mid quant interviews; fundamentals for derivative pricing |

| Market Microstructure: Bid-Ask Spread Arbitrage Question | Liquidity, execution, spreads, market impact | Medium, practical constraints and strategy design | Market data knowledge, trading experience; possible simulation | Shows trading intuition, awareness of latency, inventory and costs | Market-making, HFT, prop trading roles |

| Statistics & Hypothesis Testing: Multiple Comparisons Problem | False discovery, multiple testing corrections, overfitting | Medium, requires statistical methods and judgment | Statistical toolkits, simulations, knowledge of corrections | Reveals experimental rigor and model validation discipline | Quant researchers, data scientists, ML validation teams |

| Stochastic Calculus: Black‑Scholes Option Pricing Derivation | SDEs, Ito’s lemma, PDE derivation, risk-neutral pricing | High, advanced continuous-time mathematics | Deep math background (stochastic calculus, PDEs); time for derivation | Distinguishes senior quant talent with theoretical depth | Derivatives pricing, senior quantitative researcher roles |

| Optimization & Algorithm Design: Portfolio Optimization Problem | Convex optimization, constraints, numerical stability | Medium–High, quadratic programming and practical issues | Optimization solvers (cvxpy/CVXOPT), compute, covariance estimation | Tests practical implementation, solver familiarity, estimation risk awareness | Portfolio managers, quantitative asset allocators, PM support |

| Machine Learning & Prediction: Overfitting & Cross-Validation | Generalization, validation strategy, time-series pitfalls | Medium, diagnostic + validation design | ML libraries, historical data, compute for cross-validation | Shows production-ready ML practices and prevention of leakage | ML engineers, quant researchers using time-series models |

| Coding & Implementation: Efficient Algorithm Design | Algorithmic complexity, coding correctness, edge cases | Medium, optimal solutions require careful thought | Coding environment or whiteboard; familiarity with languages | Evaluates coding clarity, complexity analysis, implementation skill | Quant developers, software engineers, systems engineers |

| Behavioral & Domain Knowledge: Trading Loss Scenario Management | Crisis response, risk controls, communication, decision-making | Low–Medium, procedural and situational reasoning | Domain knowledge of risk systems, incident protocols | Reveals judgment, cultural fit, operational discipline under stress | Traders, risk managers, portfolio managers, operations leads |

Beyond the Questions Your Path to a Quant Offer

A quant interview rarely turns on one clever answer. Offers usually go to candidates who make their performance across the loop feel consistent with the job they are targeting.

That means probability answers should reflect risk judgment. Statistics answers should show research discipline. Coding answers should signal production reliability. Behavioral answers should sound like the candidate can protect capital, communicate clearly, and recover when a model or process breaks.

Firms notice that alignment quickly. Interviewers are not only asking, “Can this person solve the problem?” They are also asking, “Would I trust this person with live decisions, messy data, tight timelines, and incomplete information?” Candidates who state assumptions, choose a reasonable approach, and explain trade-offs tend to outperform candidates who jump to a polished but brittle answer.

Role fit matters just as much as raw technical range. A market-making seat will care more about spread economics, inventory risk, and speed under pressure. A quant research team will press harder on experimental design, multiple testing, regime sensitivity, and out-of-sample thinking. A quant developer or researcher-engineer hybrid role may give substantial weight to code quality, complexity analysis, and whether the candidate can turn an idea into something another teammate can maintain.

From a staffing perspective, placeable candidates share a pattern. They are strong enough technically to clear the bar, but they are also easy to picture on a desk or research team. They answer directly. They do not bluff through missing assumptions. They can go one layer deeper when challenged. They understand what kind of mistakes are expensive in the specific role, whether that is slippage, model leakage, unstable optimization, or operational error.

That last point affects hiring more than many candidates realize.

A candidate who solves difficult interview questions but cannot tie the answer to PnL, validation risk, or implementation cost often gets marked as interesting but hard to hire. A candidate with slightly less theoretical polish but better judgment, clearer communication, and stronger role alignment is often easier to place. Hiring managers are not buying trivia skill. They are reducing execution risk.

Nexus IT Group is one option for candidates and employers working in this space, particularly when role alignment and interview preparation need to reflect the practical realities of quant hiring instead of generic recruiting language.

Candidates exploring quant roles or employers hiring for them can connect with nexus IT group for quant recruitment support, role alignment, and practical interview guidance tied to specialized technical hiring.