There are 613 quantitative developer jobs live on Indeed right now, which matters for one simple reason: this isn’t a vague finance-adjacent niche anymore. It’s a searchable hiring market with its own expectations, screening patterns, and pay bands. On the compensation side, Levels.fyi reports a median salary of $198,000 for quant developers, a clear signal that firms pay a premium when they need someone who can write production code and understand the quantitative logic behind it (Indeed job market reference).

Most coverage still gets the role wrong. It treats quantitative developer jobs as if they sit somewhere between academic research and elite trading mystique. In practice, many of these jobs are much more concrete. Firms need engineers who can take models, market data, and execution requirements and turn them into reliable systems that work under pressure.

That distinction changes everything. It affects who gets hired, how resumes should be written, which languages matter, and where demand stems from. It also explains why strong software engineers often break in faster than mathematically impressive candidates who can’t ship reliable code.

Table of Contents

- The High-Stakes World of Quantitative Development

- What a Quantitative Developer Actually Does

- The Skills That Command a Quant Developer Salary

- Where to Find Quantitative Developer Jobs

- Quantitative Developer Salary and Career Path

- How to Prepare for a Quant Developer Interview

- Frequently Asked Questions About Quant Dev Careers

The High-Stakes World of Quantitative Development

Quantitative development sits in a narrow part of the talent market, but it’s a real one. Firms aren’t just hiring “software engineers with some finance exposure.” They’re hiring for a distinct role that exists because trading, pricing, risk, and model infrastructure break when engineering quality drops.

That’s why compensation stays high. The market rewards people who can bridge three things at once: programming discipline, numerical accuracy, and production performance. A candidate who can only do one or two of those usually doesn’t clear final rounds.

The role also carries more operational responsibility than many candidates expect. A quant developer may support model implementation, own data pipelines tied to pricing or execution logic, improve backtesting systems, and work directly with researchers or traders who care about correctness and turnaround time. The academic stereotype misses that reality.

Practical rule: The stronger framing is “high-performance software engineer in a quantitative environment,” not “junior quant researcher who happens to code.”

Hiring managers often struggle because they write the job too broadly. Candidates struggle because they position themselves too academically. Both mistakes slow down the search. The firms making good hires are usually specific about the environment, latency sensitivity, asset class, and whether the role sits closer to research tooling, trading infrastructure, or model implementation.

That’s what separates real quantitative developer jobs from generic software openings with finance keywords sprinkled in.

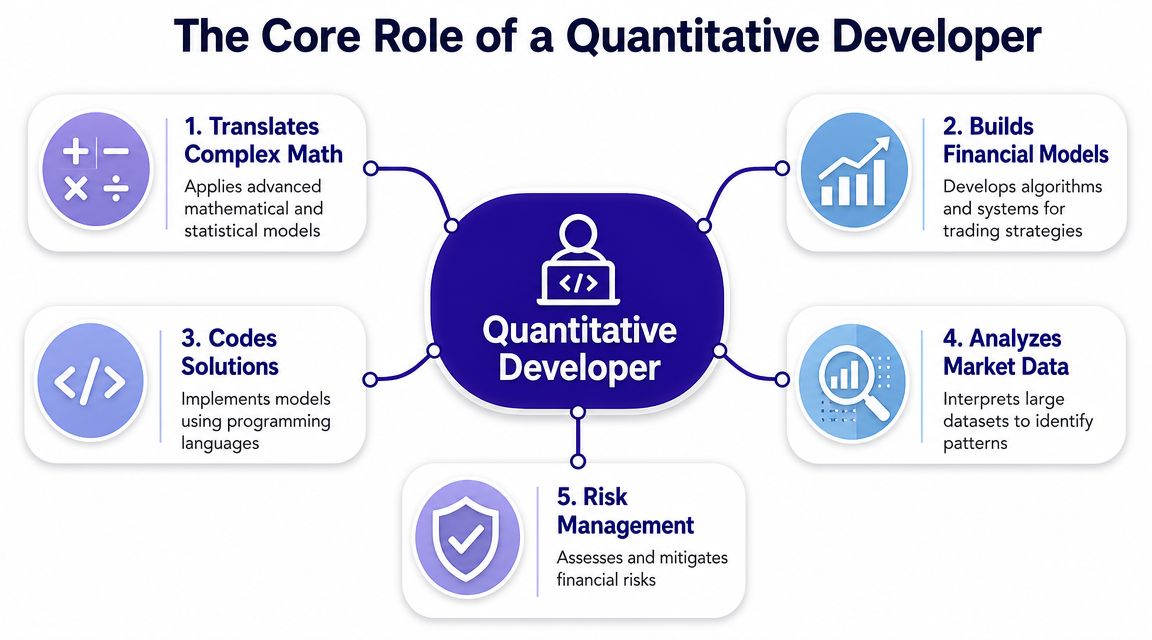

What a Quantitative Developer Actually Does

A quantitative developer builds the machinery that lets quantitative ideas operate in practice. The cleanest definition is this: the role takes mathematical or statistical models and turns them into production-grade software that can be tested, validated, deployed, and maintained.

The job is closer to engineering than research

Major banks and hedge funds consistently frame the job as a software engineering role. The core work is translating mathematical and statistical models into optimized production code, then handling implementation, backtesting and validation, and integration into trading infrastructure (Interactive Brokers quant developer roadmap).

A useful analogy is the Formula 1 engine builder. The quant researcher may design the strategy logic, but the quantitative developer makes sure the machine runs. If the implementation is slow, brittle, or inconsistent with the original model, the strategy doesn’t survive contact with production.

That’s why firms don’t treat this as a “nice to have coding” role. They expect engineering judgment. They want someone who knows when to optimize, when to standardize, when to refactor, and when a model should not go live because the infrastructure around it isn’t ready.

For candidates coming from broader trading education, a solid practical guide to algorithmic trading can help connect strategy ideas to the systems work firms hire for.

What shows up in the day-to-day work

The daily work usually includes a mix of these responsibilities:

- Model implementation: Turning research logic into maintainable code that behaves predictably outside a notebook.

- Backtesting support: Building or improving frameworks that let teams validate assumptions before capital is exposed.

- Data handling: Cleaning, normalizing, storing, and serving market data so researchers and systems use the same definitions.

- Production integration: Connecting models to order management, market feeds, risk controls, and internal services.

- Performance work: Profiling, tuning, and rewriting components when latency or throughput becomes a real constraint.

A quant developer who can’t productionize a model is usually less useful than a strong engineer with enough quantitative fluency to ask the right questions.

What the role isn’t, at least in most seats, is pure blue-sky research. Some firms do hire hybrid quant-dev profiles. But many open roles are much more operational than candidates assume. The work rewards people who like systems, precision, and accountability. It’s a build-and-own job.

The Skills That Command a Quant Developer Salary

The market doesn’t pay quant developers well because the title sounds complex. It pays for a difficult skill blend. The strongest candidates usually bring depth in one pillar and working fluency in the others. The weakest profiles try to signal everything and prove nothing.

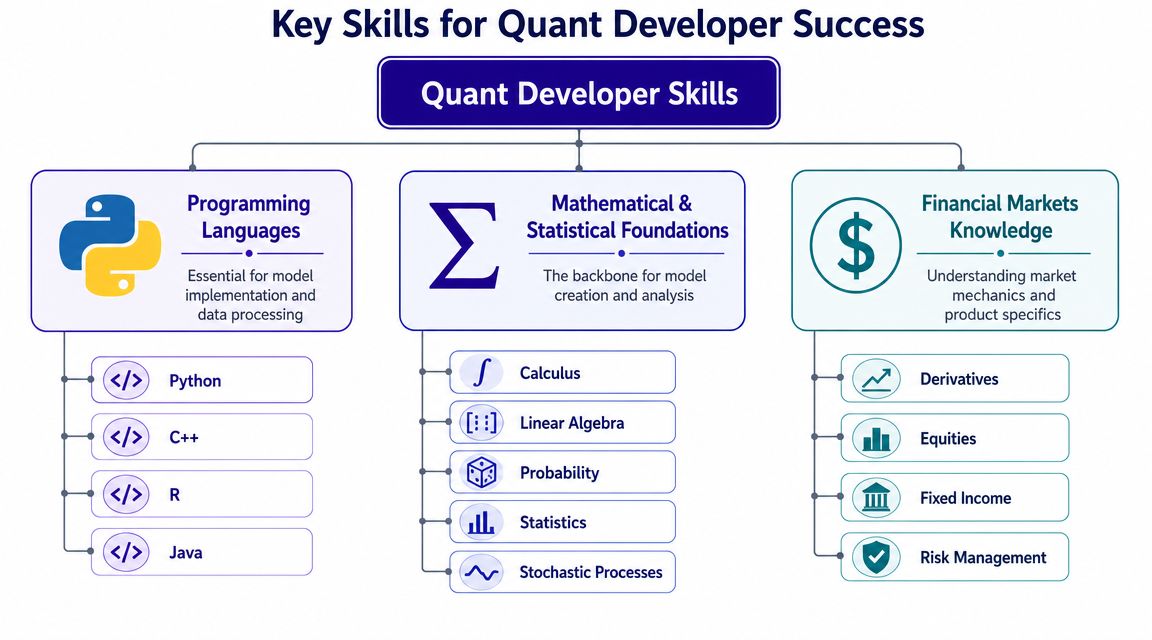

Programming languages that matter

The most practical language split in quant development is simple. C++ stays important for low-latency and trading infrastructure work. Python dominates research, prototyping, and data manipulation. That division continues to shape hiring because firms still need both fast iteration and tight production performance (QuantStart self-study plan for quant developers).

Candidates often make one of two mistakes. They either over-index on Python and underestimate how much systems work still matters, or they lead with C++ and can’t show they can move quickly with research and data tooling. Firms usually prefer someone who understands the handoff between the two.

A strong programming profile often looks like this:

- Python for implementation speed: pandas, NumPy, APIs, research tooling, testing, and internal services.

- C++ for performance-sensitive components: execution systems, latency-aware services, core libraries, and infrastructure.

- SQL for market data and analytics workflows: firms still expect developers to work comfortably with financial databases.

- Java in some environments: still relevant in parts of banking and platform-heavy infrastructure stacks.

For candidates building market intuition alongside coding skill, Rize Trade’s guide to technical analysis can be a useful supplement. It won’t replace systems knowledge, but it helps candidates understand the decision logic many models are trying to encode.

A practical roadmap for candidates who need structure is this guide on how to become a quant.

Math and statistics that earn interviews

Hiring teams usually don’t need abstract math recital. They need proof that the candidate can work with models responsibly.

That means comfort with:

- Probability and statistics: distributions, estimation, hypothesis thinking, regression logic, and model validation.

- Linear algebra: essential for many modeling and optimization workflows.

- Calculus and numerical methods: useful when models must be translated from theory into computational routines.

- Stochastic thinking: especially relevant when the desk touches derivatives, simulation, or pricing work.

What works in interviews is practical fluency. Explain why a numerical approximation was chosen. Discuss precision trade-offs. Show how assumptions affect implementation. Candidates who only name topics don’t stand out.

Financial knowledge that helps instead of distracts

Most firms don’t need a developer to sound like a portfolio manager. They need someone who understands enough market structure to avoid building the wrong thing.

Useful domain knowledge includes:

- Instrument basics: equities, futures, options, fixed income, or energy products, depending on the desk

- Workflow awareness: how data becomes signals, how signals become orders, and where risk checks sit

- Model context: what the code is trying to optimize, estimate, or forecast

- Communication with quants and traders: enough fluency to clarify assumptions quickly

The hiring edge comes from relevance. A candidate who knows the desk’s instruments and can code cleanly usually beats the candidate with broader theory and weaker implementation habits.

Where to Find Quantitative Developer Jobs

Quant developer hiring is no longer concentrated in a handful of hedge funds. Searches across major job boards and recruiter pipelines now turn up roles at banks, commodity merchants, asset managers, fintechs, and energy trading firms in addition to the usual prop and HFT names. That broader employer mix matters because it changes both the job itself and the profile that gets interviews.

I see the same mistake every quarter. Strong engineers target only marquee quant funds, ignore adjacent employers, and conclude the market is tiny. It is not. It is fragmented. A quant developer is often a high-performance software engineer working under quantitative constraints, and that description fits far more firms than the old PhD-only stereotype suggests.

The employer map has widened

Banks still hire heavily, especially for pricing infrastructure, model implementation, risk systems, and controls-heavy platforms. These roles usually reward engineers who can work inside larger codebases, document decisions clearly, and own production changes without drama.

Hedge funds and prop shops hire for a different operating style. Feedback loops are shorter. Researchers and traders sit closer to engineering. Code gets judged on usefulness, speed, and reliability very quickly.

Energy trading is where many candidates are still behind the market. Power, gas, and commodities firms need developers who can handle forecasting inputs, market data pipelines, optimization logic, and desk tooling. In practice, these teams often hire candidates who look more like strong systems or platform engineers with quantitative range than textbook academics.

Fintechs and some asset managers sit in the middle. They may be building pricing engines, analytics products, portfolio tools, or ML-backed workflows for investment teams. The environment is often less latency-sensitive than HFT, but the expectation for production discipline is still high.

How different firms hire for the role

| Firm Type | Primary Focus | Tech Environment | Compensation Structure |

|---|---|---|---|

| Hedge fund | Research enablement, strategy implementation, portfolio tools | Python-heavy with performance components, fast internal iteration | Usually strong base plus discretionary bonus |

| Prop shop | Trading systems, execution, internal tools | Tight engineering loops, performance-focused, often lower-level systems emphasis | Often more directly tied to desk performance |

| HFT firm | Latency-sensitive execution and infrastructure | C++-leaning, systems-heavy, highly optimized environments | Often premium compensation tied to specialization |

| Bank | Model implementation, validation, risk, pricing infrastructure | Larger platform ecosystems, stronger controls, more process | More structured base salary and bonus mix |

| Fintech or asset manager | Productized models, analytics platforms, data and ML infrastructure | Broader stack, cloud and platform tooling, cross-functional delivery | More varied, sometimes less bonus-driven than trading firms |

| Energy trader | Algorithmic bidding, execution modeling, market operations support | Hybrid stack with strong modeling and operational requirements | Depends on commercial model and desk exposure |

A practical search strategy follows from that table. Search by problem set, not just by title. "Quantitative developer" misses many good roles that are posted as pricing engineer, front-office developer, risk developer, model platform engineer, electronic trading developer, or commodities analytics engineer.

Current hiring also favors implementation maturity over academic signaling. Many openings ask for Python, production model integration, standardization of research code, and the ability to work across quant, risk, and engineering groups. Senior seats often want enough experience to own messy systems, not just write isolated libraries. That is one reason firms continue to pay a premium for strong low-level specialists in performance-heavy environments, especially in C++, as discussed in this breakdown of what quant firms are paying for C++ engineers.

The best candidates widen the target list early. The best hiring teams drop vague quant language and describe the actual work: pricing stack, execution tooling, risk platform, market data plant, or optimization engine. That specificity gets better applicants.

Quantitative Developer Salary and Career Path

Compensation shows how far this role has moved beyond the old "PhD-only" stereotype. In the current market, quant developers are paid like specialized engineers who can ship reliable systems under trading, risk, and model constraints. Public compensation data from levels.fyi shows software engineers at top trading firms and hedge funds earning well above standard big-tech cash compensation once bonus is included, which lines up with what hiring teams have been offering for strong quant-adjacent engineering talent in recent search cycles (levels.fyi trading and hedge fund compensation data).

What pay looks like across levels

Salary bands are only half the story. In quant development, the primary driver is scope.

Junior hires usually start with model implementation, tooling, test coverage, and support for research or desk-facing systems. The pay is strong because even entry-level work often sits close to pricing, execution, or risk workflows where mistakes are expensive. Banks and large energy firms tend to offer more structured packages. Hedge funds, prop shops, and some trading firms push more of the upside into bonuses.

Mid-level pay rises fast when a developer can own production services instead of tickets. That means handling release discipline, debugging performance regressions, improving reliability, and working directly with quants, traders, or risk managers without constant supervision. This expanded role has broadened the market. Banks still hire, but so do commodity houses, market makers, and energy traders that need engineers who can work with data, models, and live operational systems.

Senior compensation separates sharply because the job changes again. The highest-paid people are not just writing code faster. They are setting architecture, preventing bad model rollouts, reducing latency where it matters, and making judgment calls that protect revenue or limit losses.

One skill still carries a visible premium. Firms continue to pay up for low-level performance work, especially in front-office and latency-sensitive environments. This market view of what quant firms are paying for C++ engineers is consistent with what recruiters see in mandates tied to trading infrastructure and performance-critical libraries.

How careers progress in practice

The cleanest career paths usually fall into three tracks:

- Technical specialist: owning core libraries, pricing engines, platform architecture, or performance engineering

- Quant-facing builder: working closer to models, validation, and research productionization

- Team lead or manager: running delivery, setting development standards, and hiring for multi-discipline groups

The strongest careers are built on system ownership, not title collection.

A developer who can stabilize a fragile pricing stack, standardize research code for production, or improve the reliability of a risk platform usually out-earns someone with a fancier title and thinner delivery record. I have seen candidates from energy trading and bank platform teams beat out traditional hedge fund profiles because they could point to shipped systems, incident reduction, and cleaner model deployment practices.

Career upside also depends on where the seat sits relative to the business. Roles attached to revenue-generating desks, execution infrastructure, or business-critical analytics usually have better bonus potential than support-heavy seats with little commercial exposure. That does not make one path better for everyone. Some candidates should choose the bank path for training, brand, and stability. Others should choose a smaller trading environment for faster scope and pay volatility.

Firms are also getting stricter about how they assess progression. Resume screens still matter, but many teams now want clearer evidence of coding judgment, communication, and delivery under pressure. Tools for AI for candidate evaluation are part of that shift, especially in early-stage screening for high-volume engineering pipelines.

A strong quant developer career is still very achievable without a pure academic quant background. The market rewards engineers who can build fast systems, work with quantitative requirements, and hold up under production pressure. That is why this field now attracts far more than the classic PhD-to-hedge-fund profile.

How to Prepare for a Quant Developer Interview

A large share of quant developer interviews still reject candidates for plain engineering reasons. The miss is rarely advanced math. It is weak code discussion, thin system design, unclear trade-off thinking, or a resume that hides the only work that would have won the process.

Hiring teams are more practical than many candidates expect. Across hedge funds, banks, market makers, and energy trading firms, the pattern is similar. They want engineers who can work inside quantitative constraints, explain production choices, and stay credible with researchers and front-office stakeholders. That is a different preparation target from the old "PhD-only quant" stereotype, and candidates who understand that usually interview better.

Build a resume around shipped work

A strong quant developer resume reads like a record of delivered systems, not a list of topics studied. Show what you built, what constraints mattered, how you tested it, and what changed because of your work.

Good examples include:

- A backtesting engine with clear treatment of data quality, parameter handling, and reproducibility

- A pricing or simulation project where you can explain implementation choices, numerical limits, and validation

- A market data pipeline that shows you understand reliability, throughput, and failure cases

- A latency-aware C++ component where you can discuss memory, profiling, and why you accepted certain trade-offs

- A research-to-production handoff project that proves you can turn exploratory code into maintainable software

The weak version is vague. "Worked on trading models" gives a recruiter nothing to sell internally. "Built Python services for historical data normalization and strategy testing, added validation checks, and reduced rerun time" gives a hiring manager something concrete to probe.

I have seen candidates from bank platform teams and energy merchants outperform stronger academic profiles because they could walk line by line through a shipped system and defend their decisions.

For candidates who want to rehearse under more structured evaluation, tools focused on AI for candidate evaluation can help simulate timed interview conditions and sharpen communication under pressure.

Prepare for the interview loop firms run

The typical loop mixes standard software engineering with role-specific questioning. The order changes by firm, but the evaluation categories are predictable.

A serious prep plan should cover:

-

Data structures and algorithms

Many firms still use a standard engineering screen. It may be lighter than big tech, but weak fundamentals still end processes early. -

Language depth in Python or C++

Be ready to discuss performance, debugging, testing, libraries, memory behavior, and the limits of the language in production. -

System design under quantitative constraints

Stronger candidates stand out in this area. Design a market-data service, backtesting platform, or model deployment flow. Explain reproducibility, observability, failure handling, and scaling. -

Applied math and probability

The bar is usually practical. Interviewers want to know whether you can reason carefully about uncertainty, inputs, and implementation risk. -

Behavioral judgment and collaboration

Quant developers work with researchers, traders, risk, and platform engineers. Firms look for people who can clarify vague requirements, push back when needed, and still move delivery forward.

The best preparation method is to answer realistic prompts out loud, then tighten the answer until it sounds like someone who has owned production software.

Useful prompts include:

- How does a backtesting engine differ from a live execution system?

- When is Python fine in production, and when does it become a bottleneck or control risk?

- How would you verify that a model implementation matches the research specification?

- What fails first in a market-data pipeline during a volatile session?

- How do you handle conflicting demands from a quant researcher and a production engineering lead?

Candidates who need a tighter prep checklist can use curated quant interview questions and hiring guidance.

The best interview answers sound operational. They include trade-offs, failure cases, test strategy, and what you would do if the first version broke under load.

Frequently Asked Questions About Quant Dev Careers

Does a quant developer need a PhD

A PhD helps for research-heavy seats, especially on pricing, systematic strategy research, or model design. It is not the default requirement for quant developer hiring. In practice, I see far more offers go to candidates with strong software engineering skills, solid math judgment, and evidence they can ship production code under tight performance and reliability constraints. Bachelor's and Master's candidates get hired every week if they can show that mix.

The market has also widened. Banks, market makers, and energy trading firms often care more about systems ability than academic pedigree.

What's the difference between a quant developer and a quantitative analyst

The split is usually ownership. Quantitative analysts tend to own research, model logic, and strategy development. Quant developers own implementation, performance, testing, integration, and production support.

Some firms blur the line, especially smaller funds. In larger organizations, they are usually separate hiring tracks with different interview loops and different success metrics. A quant analyst gets judged on model quality and research output. A quant developer gets judged on whether the system is correct, fast, observable, and reliable when markets get messy.

Which language should a beginner learn first

Python is the best first step for most candidates because it shows up across research tooling, data workflows, and internal analytics. It also lets candidates build useful projects fast, which matters more than collecting certificates.

That said, Python alone rarely closes the loop for front-office quant dev roles. Candidates who want low-latency, execution, or core platform work should add C++ sooner rather than later. Java still shows up in bank infrastructure and some trading platforms. SQL remains standard because a lot of the job still involves getting the right data, verifying it, and tracing what broke.

Are quantitative developer jobs only in hedge funds

No. Hedge funds are only one part of the hiring market.

Banks still hire heavily for pricing infrastructure, risk systems, market data, and electronic trading support. Energy and commodities firms have expanded demand too, especially for developers who can handle optimization, real-time data flows, and integration with trading and risk platforms. That broader demand matters because it gives strong engineers more entry points than the old PhD-to-hedge-fund story suggests.

What gets candidates rejected most often

The fastest rejection usually comes from one of three gaps. Weak core engineering. Vague project descriptions that sound academic instead of operational. Poor answers on trade-offs.

Hiring teams are trying to separate people who have read about quant systems from people who have built them. If a candidate cannot explain why they chose a design, how they tested it, where it would fail under load, or what they would monitor in production, the process usually ends there. Firms can teach desk context. They are much less willing to teach engineering discipline from scratch.

Teams that need quant talent often lose time at the definition stage. They know they need stronger model implementation, better trading infrastructure, or sharper engineering around data and execution, but the job spec stays fuzzy and the candidate flow goes sideways. nexus IT group works on specialized technology hiring, including quant recruitment, which makes it a practical option for employers trying to fill hard-to-define quantitative developer roles and for candidates who want clearer alignment between their background and the market.