A private equity associate can earn a first-year all-in package of approximately $275,000 to $390,000 at top firms, and at the most elite funds that figure can exceed $400,000 according to Wall Street Prep’s private equity salary breakdown. That headline gets attention, but it also hides the harder truth: private equity associate careers are narrow-entry, high-pressure roles built for people who can evaluate risk, move fast under imperfect information, and execute cleanly when the room gets crowded.

The barrier to entry is just as important as the upside. The role is data-centric, firms typically require at least two years of investment banking analyst experience, and despite a nationwide average salary of roughly $99,000 in 2022, entry-level associates at many firms still land six-figure first-year pay, as outlined by Investopedia’s guide to becoming a private equity associate. For anyone trying to understand how the economics of funds connect to career incentives, a working grasp of PE fund entities and waterfalls helps explain why firms pay aggressively for disciplined execution talent.

Much career content stops too early. It tells candidates how to interview, but not how to survive the first year. It tells finance graduates how to break in, but not how a technology leader can build a high-impact career inside the PE ecosystem. And it rarely helps PE-backed companies hire the kind of technical operators who can drive value creation after the deal closes.

Table of Contents

- An Introduction to Private Equity Careers

- The Private Equity Associate Role Explained

- Your Roadmap to Becoming a PE Associate

- PE Associate Compensation and Career Progression

- Common Exit Opportunities and Long-Term Paths

- A Guide for Tech Talent and PE-Backed Firms

- Conclusion Is a PE Associate Career Right for You

An Introduction to Private Equity Careers

Private equity attracts candidates who want a sharper seat at the table than most corporate jobs offer. Associates don’t just report numbers. They test assumptions, pressure valuations, support diligence, and help determine whether capital should go into a business at all.

That’s why private equity associate careers remain so competitive. The field rewards people who can combine technical accuracy with judgment. A clean model isn’t enough. Firms want candidates who can explain what drives returns, where downside risk sits, and why one target deserves more attention than another.

What firms are actually buying

Most firms aren’t hiring raw potential. They’re hiring pre-trained execution capacity.

The standard profile is someone who already knows how to work through deal materials, organize a process, manage comments under pressure, and stay precise late at night when the quality bar hasn’t moved. Banking analysts fit that mold because they’ve already been screened on stamina, attention to detail, and transaction reps.

A strong candidate usually brings:

- Transaction exposure: Live deal experience matters because PE teams don’t want to teach the basics from scratch.

- Analytical fluency: Associates need to be comfortable moving from raw data to an investable view.

- Commercial judgment: The best hires don’t just explain a company. They form a point of view.

- Professional restraint: Teams notice candidates who are confident without being loud.

Practical rule: PE firms rarely pay for promise alone. They pay for proof that a candidate can handle ambiguity, speed, and scrutiny.

Why the career is so sought after

The appeal isn’t just compensation. It’s proximity to decision-making.

Associates often sit close enough to senior investors to see how a deal thesis changes under lender pressure, management questioning, or a tougher diligence finding. That kind of exposure compounds fast. It’s one reason candidates who can break in often stay in the broader PE ecosystem even if they don’t remain in the exact same seat long term.

For technology professionals, the opening is different but still real. The direct path into an investment associate role is narrow. The path into PE-backed companies, value-creation teams, technical diligence support, and operating roles is far more realistic and often more strategically important.

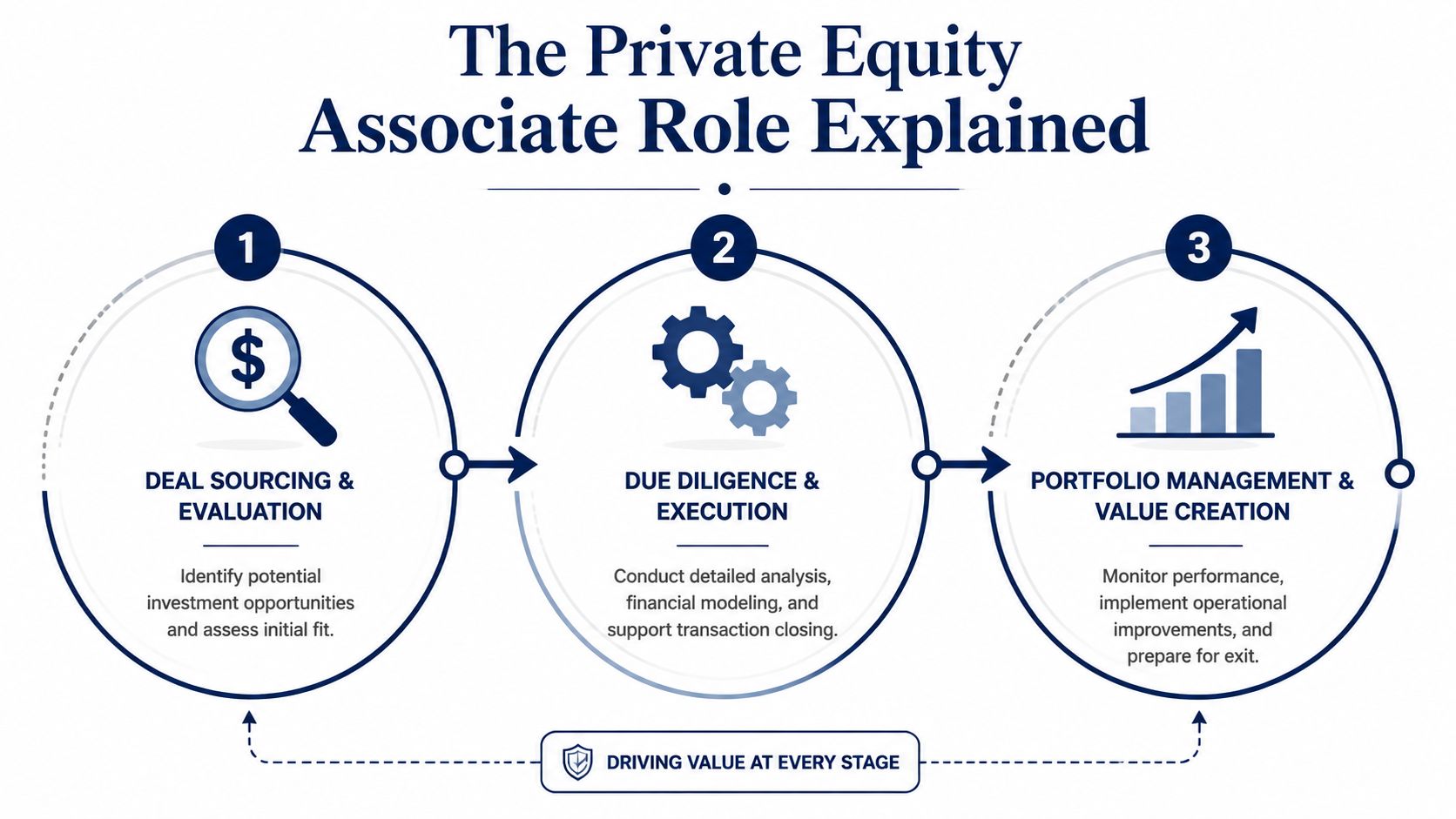

The Private Equity Associate Role Explained

The associate is the deal quarterback. Not the final decision-maker, and not the person setting fund strategy, but the person who keeps the work moving, makes sure the details reconcile, and turns scattered diligence into something partners can underwrite.

The role demands advanced technical proficiency in LBO modeling and CIM review. Associates are the primary analytical engine for deal execution and routinely build complex LBO models, with firms explicitly requiring prior banking experience where those skills are developed, as described in this private equity career path overview.

Why associates become the deal quarterback

A good associate translates noise into decisions. CIMs arrive polished. Management presentations tell a favorable story. Quality of earnings reports answer some questions and create others. Associates sit in the middle and have to sort signal from salesmanship.

That’s why the role is more than spreadsheet work. Yes, the model matters. But so does knowing which assumptions deserve pressure, which customer concentration issue is manageable, and which operational weakness turns a “fixable” story into a bad risk.

For candidates coming from banking, the closest adjacent skill set is strong transaction execution plus the ability to discuss why a deal works, not just how it closes. For candidates trying to sharpen that technical side, merger and acquisition modeling resources can help build fluency around the mechanics PE interviews usually probe.

The three working lanes of the role

The work usually falls into three lanes, and each one tests a different muscle.

| Lane | What the associate does | What separates strong performers |

|---|---|---|

| Deal evaluation | Reviews CIMs, screens opportunities, builds initial views on fit | Spots weak assumptions early |

| Due diligence and execution | Builds models, coordinates workstreams, pressure-tests downside | Keeps speed without losing precision |

| Portfolio oversight | Tracks performance, supports add-ons, monitors business health | Connects operations to investment outcomes |

The first lane is screening. A firm may look at many opportunities, but only a subset deserve serious time. Associates help narrow that list by checking whether the business fits the mandate, whether the industry structure makes sense, and whether the valuation can support acceptable returns.

The second lane is diligence and execution, where long hours are justified. The team is moving through legal, accounting, commercial, financing, and management diligence in parallel, and mistakes become expensive quickly.

The third lane is portfolio management. Associates often support monitoring of portfolio companies, review financial performance, and help evaluate bolt-on acquisitions. That work teaches an important lesson early: buying a company is only the start. Value creation depends on what happens after closing.

The best associates don’t just build a model that works. They build one that exposes where the deal could break.

Your Roadmap to Becoming a PE Associate

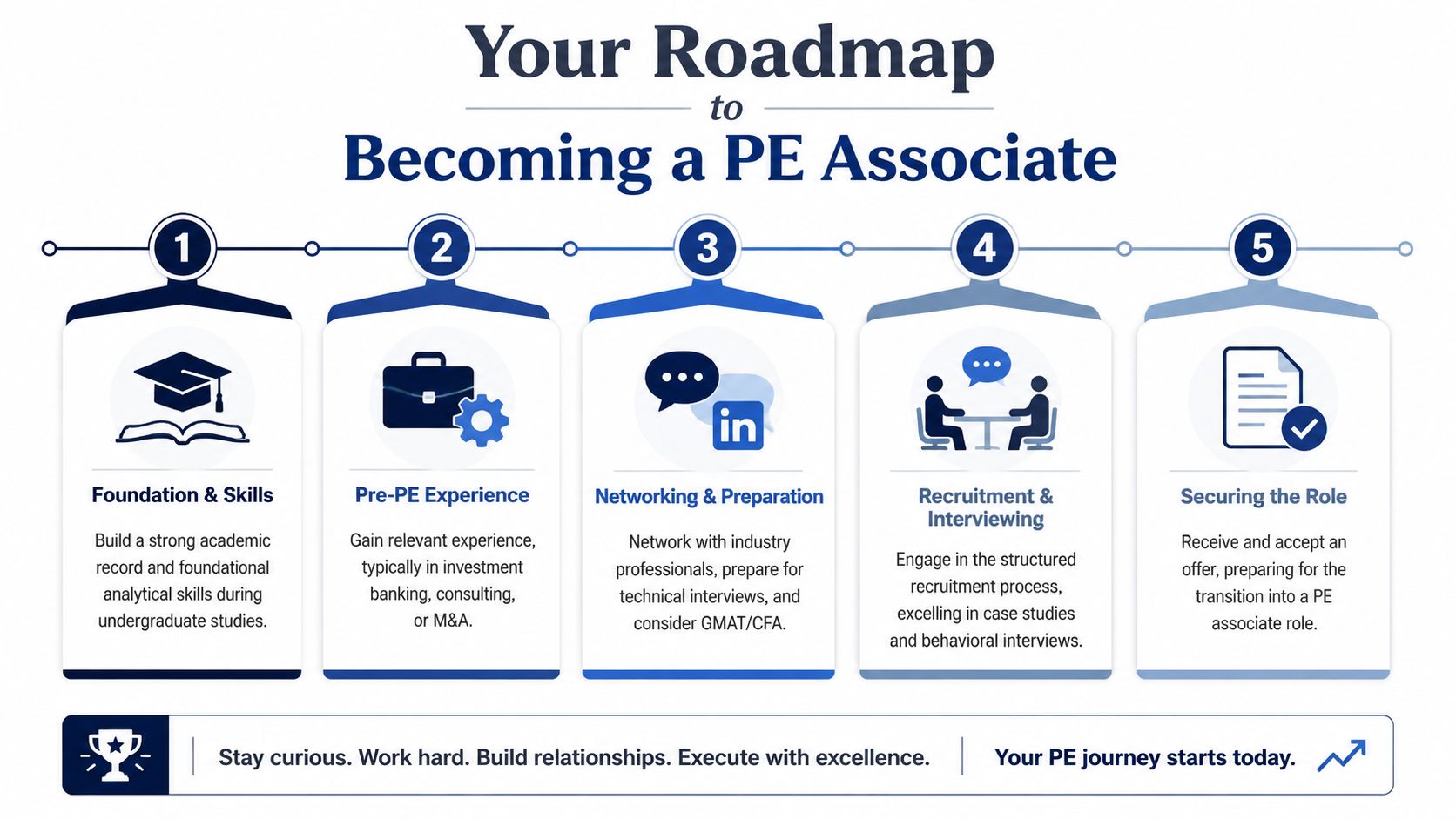

Breaking in is less about generic ambition and more about sequence. Candidates who win offers usually prepare before the market asks for it, not after a recruiter calls.

What to build before recruiting starts

The first checkpoint is background. Most firms want prior transaction training, and many prefer investment banking because it gives them a known skill baseline.

Candidates should focus on four assets before they ever interview:

-

A credible deal sheet

Not every listed deal will matter. The ones that matter are the deals a candidate can explain cleanly, including business model, valuation logic, financing structure, and key risks. -

A working LBO toolkit

Interviewers don’t need textbook definitions. They want to see that a candidate can move from assumptions to returns without getting lost in mechanics. -

Commercial opinions

A candidate should be able to answer simple but uncomfortable questions. Is this industry attractive? Why now? Why this company and not a competitor? -

A disciplined network

PE recruiting still runs through headhunters, direct outreach, alumni channels, and informal references. Candidates who wait until a process opens are late.

A practical way to think about preparation is to behave like an investor before having the title. Read filings and debt documents. Pull apart investor presentations. Rebuild transaction logic independently. Compare management narratives with operating realities.

How to handle interviews and the first year

Interviews usually test three things at once: technical competence, investment judgment, and fit under pressure. Strong candidates prepare for all three.

A useful prep stack includes:

- Timed modeling work: Practice building under time pressure, not in ideal conditions.

- Paper LBO drills: Learn to simplify quickly and defend assumptions verbally.

- Deal walkthroughs: Pick a few deals and know them in depth.

- Behavioral answers: Show maturity, not polished slogans.

For candidates who need support on recruiter mapping, process timing, and market context, private equity recruiter guides can clarify how firms and search professionals structure the funnel.

The first-year adjustment is where many otherwise strong hires stumble. Technical skill gets someone through the door. Political timing keeps them there.

“For the first few months, it is better to listen. Even if you were a rockstar analyst, no one wants to hear your opinion.” That advice comes directly from a veteran in this Wall Street Oasis discussion on first-year associate dos and don’ts.

That advice sounds old-fashioned, but it’s operationally correct. New associates often join teams with hard-wired habits, informal power structures, and unwritten style preferences around how comments are handled, when updates get escalated, and who wants detail versus synthesis.

A practical first-year checklist looks like this:

- Learn partner preferences early: Some seniors want a concise answer first. Others want to see every assumption.

- Fix small errors fast: Teams forgive inexperience more than they forgive repeated sloppiness.

- Don’t posture as an investor on day one: Credibility usually comes after clean execution.

- Speak up once the work earns attention: Silence forever isn’t the goal. Timing is.

Candidates often think the hard part is landing the offer. In reality, a big part of succeeding in private equity associate careers is understanding when to contribute, how to absorb feedback without drama, and how to stay sharp when every draft carries consequences.

PE Associate Compensation and Career Progression

Compensation draws attention because the numbers are high. Career staying power comes from understanding how those numbers are earned, when they hold up, and what changes as an associate becomes more valuable to the firm.

Earlier compensation data in this article already covered the top end of the market. The practical point is simpler. Associate pay varies sharply by fund size, strategy, geography, and bonus philosophy, so candidates should treat headline figures as a range, not a promise. I tell candidates to ask two separate questions during process: what did last year’s associates make, and how discretionary was that outcome?

How pay is structured

Most firms pay associates through base salary plus annual bonus. The difference is in how much confidence a candidate should have in the bonus.

According to DocuBridge’s private equity career path summary, some major-market firms show base salaries from $150,000 to $300,000 and bonuses from 100% to 300% of base. Those numbers usually reflect the upper end of the market, not the median outcome across all platforms.

The compensation picture gets clearer when broken down by firm type:

2026 Private Equity Associate Compensation (All-in, Year 1)

| Firm Type | Base Salary Range | Bonus Range (% of Base) | All-in Compensation |

|---|---|---|---|

| Top private equity firms | $135,000 to $155,000 | 100% to 150% | $275,000 to $390,000 |

| Elite funds | Qualitatively similar base structure, with stronger upside | Can push above standard top-firm ranges | Exceeds $400,000 |

| Major markets broadly | $150,000 to $300,000 | 100% to 300% | Varies with firm and performance |

| Mid-market firms | $130,000 to $150,000 | Floor-guaranteed at 100%, rarely above 125% of target | More predictable than top-end upside |

| Lower-tier firms | Lower than top and mid-market structures | 50% to 100% | Lower all-in outcomes |

| Nationwide average for less than three years of experience in 2022 | Not broken out here by base and bonus | Not specified | Roughly $99,000 |

Mid-market compensation gets misunderstood because candidates often focus on the biggest number on the page. In practice, some standard mid-market firms offer a better risk-adjusted package. As discussed in this Wall Street Oasis thread on associate bonus variance, floor-guaranteed bonuses around 100% of base salary and base salaries between $130,000 and $150,000 can make total compensation more predictable, even if the ceiling is lower.

That trade-off matters for technology operators considering a move into PE-backed environments. A software leader joining a portfolio operations team or strategy function may not match fund-level upside in year one, but the path can offer clearer operating ownership, broader remit, and a more direct route into the kind of value-creation work described in this operating partner playbook for private equity success.

What promotion really depends on

Associates usually spend 2 to 3 years in the role before moving up, according to Wall Street Careers’ guide to the private equity associate path. That timeline is only a rough benchmark.

Promotion decisions are tied to judgment, trust, and repeatability under pressure.

A candidate on track for senior associate or vice president usually shows four things:

- Independent execution: They can run a workstream without constant correction.

- Better commercial judgment: They identify the issue that matters before the room points it out.

- Team management: They can review analysts or junior associates without creating extra work for senior staff.

- Credibility with management and internal stakeholders: Their work holds up in a partner meeting and in front of a portfolio company CFO.

The role changes as those skills build. Early associate years are heavily weighted toward modeling, diligence support, committee materials, and process management. Later, the center of gravity shifts toward investment judgment, management interaction, and influence over how the deal team frames risk and value creation.

Hiring managers at PE-backed companies should pay attention to that shift. The best associates are not just spreadsheet technicians. They are often strong candidates for strategy, finance, transformation, and product-adjacent operating roles because they have spent years seeing how investors evaluate growth, margin pressure, technical debt, and execution risk.

A simple screening rule helps. Candidates who talk only about comp often struggle with the actual job. Candidates who talk about judgment, responsibility, and operating exposure usually have a better shot at advancing.

Common Exit Opportunities and Long-Term Paths

A private equity associate role is valuable partly because it compounds into several credible next steps. Some are obvious. Others are underused and often better aligned with a person’s skill set.

The classic paths

The most direct route is to stay in private equity. Associates who perform well can remain on the investing track and move toward vice president, principal, and eventually partner-level responsibilities.

Other candidates use the role as a launch point into adjacent investment seats. Common moves include hedge funds, venture capital in selected cases, or another PE fund with a different strategy, sector, or fund size. Some leave for business school if they want brand reset, network expansion, or a cleaner pivot to a different platform.

These exits tend to favor people who can point to more than hours worked. Recruiters look for candidates who can explain how they assessed opportunities, where they influenced the process, and what they learned from businesses that performed differently than expected.

Why portfolio company roles matter more than many candidates think

The strongest overlooked path is into a PE-backed operating company.

That might mean strategy, finance, business operations, revenue operations, product leadership, cybersecurity, data, or technology modernization. The appeal is simple. It puts someone closer to implementation. Instead of debating the model, they help create the operational result the model was underwriting.

For candidates interested in that route, understanding how PE firms think about operating leadership helps. This operating partner playbook is useful context because it shows the traits firms value when they need operators who can convert an investment thesis into measurable execution.

A practical way to evaluate exits is to ask one question: does the next role increase ownership of outcomes?

- Staying in PE increases ownership of investment judgment.

- Joining a portfolio company increases ownership of execution.

- Moving into another fund type changes the investing style and decision horizon.

- Going to corporate strategy or consulting broadens business exposure but can reduce direct capital allocation authority.

Candidates who understand that trade-off make better long-term decisions than candidates who chase prestige labels alone.

A Guide for Tech Talent and PE-Backed Firms

Over 70% of PE firms hiring for traditional associate roles ask for prior investment banking experience, according to the existing source cited earlier in this article. That matters for technology professionals because it explains why a direct switch into a classic fund seat is uncommon. It also explains why many strong candidates miss the more realistic path. The better entry point is often the portfolio company, where the core work of value creation happens.

For engineers, product leaders, data specialists, cloud architects, and cybersecurity professionals, PE-backed companies can be a strong fit if they want business impact, faster decision cycles, and exposure to board-level priorities. The trade-off is real. These environments usually offer more scope and visibility than a large enterprise role, but less structure, thinner teams, and less patience for projects that do not tie back to revenue, margin, risk reduction, or exit readiness.

That distinction matters in hiring.

A PE-backed business rarely needs a technologist just to keep systems running. It needs someone who can clean up a messy ERP environment after an acquisition, shorten reporting cycles so leadership can trust the numbers, reduce security exposure before a sale process, or help a product team focus on features that support retention and pricing power. Candidates who present themselves as pure technical experts often lose to candidates who can explain operating impact in plain English.

Tech candidates who break in tend to do four things well:

- They target the right seat. Portfolio company roles in product, data, security, enterprise applications, and engineering leadership are often more attainable than fund roles.

- They translate technical work into investment outcomes. “Migrated infrastructure to the cloud” is weak. “Cut downtime, improved deployment speed, and reduced support cost” gets attention.

- They understand the sponsor context. A company held by a growth-oriented sponsor hires differently from one owned by a turnaround fund.

- They show comfort with pace and scrutiny. PE-backed leadership teams track progress closely. Weekly visibility is common, and weak prioritization gets exposed fast.

The same pattern shows up on the employer side. PE-backed firms often lose strong technical candidates because the interview process signals confusion. The brief says “modernize the platform,” but no one can explain the current stack, the budget, the sequencing, or how much authority the hire will have. Good candidates read that correctly. They assume they will inherit political risk without decision rights.

Hiring managers can avoid that mistake with tighter role design.

| Hiring issue | What loses strong tech candidates | What works better |

|---|---|---|

| Role definition | Broad transformation language with no scope | A specific 6 to 12 month mandate tied to business goals |

| Executive alignment | Mixed messages from CEO, CFO, and product or tech leaders | Clear agreement on priorities, budget, and reporting lines |

| Interview process | Panels that test for brilliance but not operating fit | Interviews that assess execution, communication, and change leadership |

| Offer pitch | Compensation only | Compensation plus mandate, sponsorship, team quality, and room to make decisions |

I tell clients to hire for translation skill, not just technical depth. The best PE-backed technology leaders can explain architecture, risk, and delivery choices in terms a CFO, operating partner, or board member can act on. That is especially important in businesses going through carve-outs, integrations, pricing changes, or aggressive growth plans.

Cultural fit is usually where the deal gets won or lost. A senior engineer from a large public company may accept intensity, but still reject a role if leadership treats technology as a cost center and expects transformation without headcount, process discipline, or executive sponsorship. PE-backed companies that attract top tech talent are candid about the mandate, the constraints, and what success looks like in the first year.

Specialized recruiting support can help here. Firms such as Nexus IT Group work on technology hiring across AI engineering, cloud, cybersecurity, software, and IT leadership, which is relevant when a PE-backed company needs candidates who can operate in an investment-driven business rather than a standard enterprise IT function.

For technology professionals, the practical question is not whether private equity will hire them into a fund tomorrow. It is whether they can step into a PE-backed business and own outcomes that matter to investors. For hiring managers, the question is just as direct. Can the company offer enough clarity, sponsorship, and real authority to convince top technical talent to take on a hard mandate?

Conclusion Is a PE Associate Career Right for You

Private equity associate careers are attractive for good reasons. The compensation can be exceptional. The learning curve is steep. The exposure to high-stakes decision-making is hard to match early in a career.

But the trade-offs are real. The work can be narrow before it becomes broad. The pace can be brutal. The margin for error is small, and the job often rewards restraint, judgment, and endurance as much as raw intelligence.

The better question isn't whether private equity is prestigious. It's whether the daily work fits the kind of career a candidate wants to build.

A strong fit usually sounds like this:

- They like pressure with accountability.

- They want decisions tied to capital allocation.

- They don't mind detail-heavy work when outcomes are critical.

- They can handle demanding feedback without losing composure.

A weaker fit usually shows up when someone wants the title, the pay, or the brand, but not the actual operating conditions that come with the job.

For technology professionals, the conclusion may be slightly different. The right move may not be an associate title inside a fund. It may be a role inside a PE-backed company where technical leadership has direct impact on growth, integration, security, and exit readiness.

The best career decisions in this market come from clarity, not glamour. Candidates should assess where they do their strongest work, how much ambiguity they can handle, and whether they want to analyze value, build value, or eventually do both.

If a PE-backed company needs technical leaders who can deliver under investor scrutiny, or if a technology professional wants help finding roles where operating impact matters, nexus IT group is one option for connecting specialized tech talent with hiring teams navigating growth, integration, and transformation.