Carnegie Mellon's quantitative finance program draws a sharp line between baseline competence and standout talent: top candidates are expected to bring deep command of stochastic calculus, statistics and probability, applied mathematics, programming in Python, Java, R, C++, or MATLAB, plus numerical analysis, while also showing communication, teamwork, creativity, and a trader's mindset, according to Carnegie Mellon's guide to becoming a quant. That alone answers a big part of what skills separate a good quant from a great one. The differentiator isn't one elite trick. It's a balanced skill portfolio.

That portfolio matters because the job isn't just model building. A quant has to turn noisy data, incomplete assumptions, and changing market conditions into decisions a desk can trust. In practice, the strongest people combine technical depth, coding speed, production discipline, and the ability to explain trade-offs to non-quants without watering down the logic.

For hiring managers, that changes the interview target. The best candidates won't always be the people with the flashiest math pedigree or the longest GitHub profile. For aspiring quants, it changes the development plan too. Chasing a checklist usually produces narrow specialists. Building a skill portfolio produces people who can survive, adapt, and lead.

At Nexus IT Group, those are the patterns that consistently separate solid quantitative talent from the people firms fight to hire.

Table of Contents

- 1. Advanced Mathematical and Statistical Modeling

- 2. Software Engineering and Systems Design Excellence

- 3. Machine Learning and AI Applied to Financial Markets

- 4. Deep Understanding of Market Microstructure and Liquidity Dynamics

- 5. Intellectual Curiosity and Independent Research Capability

- 6. Risk Management and Portfolio Optimization Expertise

- 7. Institutional Communication and Stakeholder Management

- 8. Adaptability and Rapid Skill Acquisition in Evolving Technology

- 8-Skill Comparison: Good vs Great Quants

- From Good to Great Building Your Quant Edge

1. Advanced Mathematical and Statistical Modeling

Strong quants know the theory. Great quants know where theory breaks.

Carnegie Mellon points to a demanding baseline: mastery of stochastic calculus, statistics and probability, applied mathematics, programming, and numerical analysis, alongside communication and creativity, as outlined in its overview of the quant path. That mix is why advanced modeling still sits at the center of the profession. Without it, a candidate can implement existing ideas but usually can't generate durable new ones.

The practical difference shows up in model selection. A good quant can price a derivative, estimate a factor exposure, or fit a time-series model. A great quant can explain when a clean model becomes dangerous because the assumptions no longer match liquidity, volatility clustering, or structural breaks in the market.

Models that survive contact with markets

The strongest modeling work usually has three traits:

- Clear assumptions: The quant can state what must be true for the model to work.

- Practical limits: The quant knows when approximation error matters and when it doesn't.

- Regime awareness: The quant tests behavior across very different market conditions, not just one favorable window.

Renaissance Technologies, D. E. Shaw, Citadel, and Two Sigma are often discussed as examples of firms built on deep mathematical thinking. The lesson isn't that every team needs exotic models. It's that real edge usually comes from adapting mathematics to a specific trading problem instead of copying a textbook formula into a backtest.

Practical rule: Complexity should earn its keep. If a simpler model is easier to monitor, explain, and maintain, it may be the better production choice.

Hiring Manager Tip: Ask candidates to walk through a model they built that failed, not just one that worked. The useful signal is whether they can identify the broken assumption quickly and discuss how they would redesign the approach.

Candidate Action Step: Rebuild one standard model from scratch, then write a short memo explaining where it would fail in live trading. That exercise develops the judgment behind what skills separate a good quant from a great one.

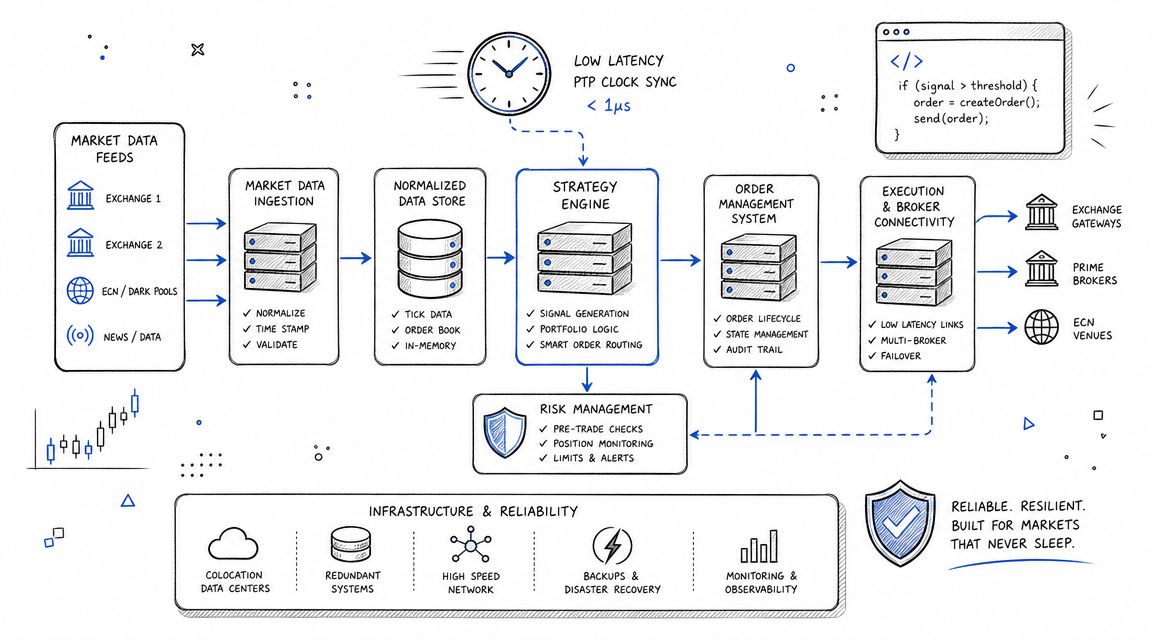

2. Software Engineering and Systems Design Excellence

A profitable backtest with brittle code isn't an asset. It's a liability waiting for market open.

In a long-form quant career guide, the common thread across quant trader, analyst, and researcher roles is being “really good at solving hard problems fast,” with data structures, algorithms, probability, statistics, machine learning, linear algebra, multivariable calculus, and Python and C++ highlighted as core foundations in this quant career discussion on YouTube. That point matters because modern quant work lives inside codebases, deployment pipelines, and production systems, not just research notebooks.

Production quality changes the value of a model

Firms like Jump Trading, Hudson River Trading, Optiver, Virtu Financial, and Citadel don't treat engineering as support work. They treat it as part of the edge. Low-latency execution, fault tolerance, observability, and sane rollback procedures can matter just as much as the signal itself.

That doesn't only apply to high-frequency shops. Even slower strategies fail when data pipelines drift, stale parameters sneak into production, or a backtest environment differs too much from the live stack.

A few habits separate real engineering from research code:

- Explicit interfaces: Inputs, outputs, and assumptions are explicit.

- Operational visibility: Logs, alerts, and monitoring catch failures early.

- System realism: Backtests mirror production constraints as closely as possible.

Teams that want stronger quant hiring should evaluate candidates the way they evaluate engineers. That means code reviews, architecture discussion, and debugging exercises, not just brainteasers. Candidates coming from a pure research background often benefit from studying software engineering career fundamentals and the discipline behind strategic software design for AI, because the same design habits carry into trading infrastructure.

Good quants write code that works. Great quants write code that still works when markets get ugly, dependencies change, and someone else has to maintain it six months later.

Hiring Manager Tip: Put candidates in front of a small broken system and ask them to diagnose it. Debugging quality reveals more than polished whiteboard answers.

Candidate Action Step: Turn one personal strategy into a production-style project with tests, configs, logging, versioned data assumptions, and deployment notes. That's how engineering maturity becomes visible.

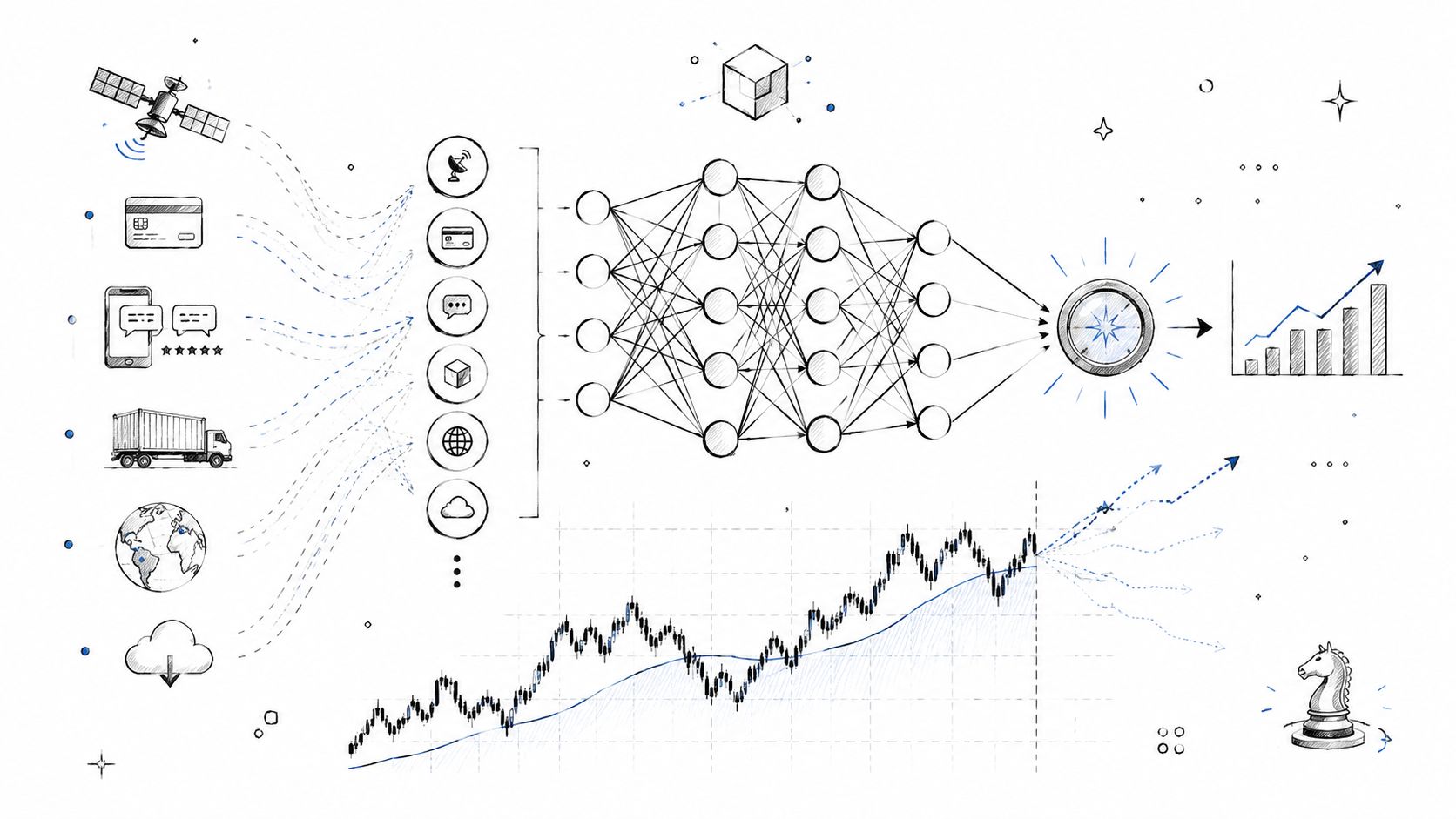

3. Machine Learning and AI Applied to Financial Markets

Machine learning has become part of the quant toolkit, but it still punishes sloppy thinking.

The gap between good and great quants here isn't who knows the most model families. It's who can decide when machine learning adds signal and when it only adds variance, cost, and false confidence. Two Sigma, Man Numeric, Bridgewater, Winton, Jane Street, and Cerebellum Capital are often cited in discussions of ML-heavy quantitative research, yet the practical lesson is simple: better prediction methods don't excuse weak data hygiene or poor market reasoning.

ML judgment matters more than ML enthusiasm

A quant with mature ML instincts usually does a few things differently. They preserve temporal order in training and testing, they look for feature leakage aggressively, and they start with simple benchmarks before escalating to more complex architectures.

That discipline matters because financial data is full of traps. Correlation can be unstable. Regimes shift. Features that look brilliant in sample often degrade quickly when conditions change.

Useful development patterns include:

- Start simple: Logistic regression, linear models, and tree-based methods often expose whether there's signal at all.

- Respect the clock: Validation schemes should reflect how the strategy would be deployed.

- Monitor decay: Every model needs a plan for drift, retraining, and retirement.

There's also a hiring reality here. Many candidates can discuss transformers, embeddings, or deep learning at a high level. Far fewer can explain why a simpler baseline may outperform in a noisy market setting, or how to detect that a model is learning market structure artifacts instead of tradable information. Candidates targeting this lane should also understand adjacent market demand around AI talent, including how firms think about roles such as AI engineer compensation in the U.S., because quant and AI recruiting increasingly overlap.

Hiring Manager Tip: Ask for an example of a machine learning project the candidate decided not to pursue. The decision quality matters as much as the implementation.

Candidate Action Step: Build one forecasting project with a naive baseline, a linear baseline, and one more complex model. Then compare error behavior, drift, and operational burden. That process sharpens judgment faster than jumping straight to deep learning.

4. Deep Understanding of Market Microstructure and Liquidity Dynamics

A model can look elegant at daily frequency and still lose money the moment it meets a real order book.

Despite knowing the math and the code, many otherwise strong quants stall because they don't understand how fills happen, why spread widens, what queue position means, or how venue rules change execution quality. Great quants do.

Theoretical edge can disappear at the point of execution

Market microstructure is where abstract alpha turns into implementation reality. Firms such as Optiver, Jump Trading, Virtu Financial, and Citadel are known for treating execution and liquidity behavior as first-order concerns, not afterthoughts. That mindset matters well beyond high-frequency trading.

A few recurring blind spots separate weaker and stronger practitioners:

- Ignoring impact: A signal isn't useful if entering and exiting destroys the economics.

- Ignoring venue behavior: Different venues and instruments impose different constraints and incentives.

- Ignoring participant behavior: Market makers, hedgers, retail flow, and institutional execution all shape what a strategy is interacting with.

A candidate doesn't need to be a pure microstructure specialist to be valuable. But they do need to understand that slippage, queue dynamics, and adverse selection can break an otherwise attractive strategy. A simple way to build that intuition is to study execution examples and practical primers such as this guide to trading slippage, then compare those frictions against one's own backtests.

If the backtest assumes frictionless execution, the strategy hasn't been tested. It's been fantasized about.

Hiring Manager Tip: Give candidates a strategy with attractive headline returns and ask what execution assumptions could invalidate it. The best answers usually come from people who've watched live trading behave badly.

Candidate Action Step: Spend time with high-resolution trade and order book data, even on a small personal project. Track where expected edge disappears between signal generation and execution.

5. Intellectual Curiosity and Independent Research Capability

Great quants rarely wait to be handed the next idea. They generate pipelines of questions on their own.

That doesn't mean chasing every shiny object. It means maintaining an active research habit: reading papers, testing hypotheses, learning adjacent methods, and keeping enough skepticism to throw most ideas away. Firms built around sustained research cultures tend to value this trait because crowded strategies don't stay special for long.

Research habits show up in idea quality

Independent research is less about brilliance than about process. The strongest researchers keep notes on hypotheses, define what would falsify an idea, and distinguish quickly between an interesting pattern and a tradable one.

Examples from across the industry point in the same direction. Teams associated with Renaissance Technologies, Two Sigma, and other research-heavy firms are often described as continuously exploring new data, methods, and cross-disciplinary ideas. The practical takeaway is that edge compounds when curiosity is structured.

A healthy research routine often includes:

- Deliberate reading: Papers, technical blogs, market structure notes, and implementation write-ups.

- Idea triage: Most concepts should be rejected quickly and cheaply.

- Cross-pollination: Useful ideas often come from adjacent fields, not just finance.

For candidates, this is one of the easiest differentiators to make visible. A thoughtful research log says more than a vague claim of being “passionate about markets.” Hiring teams can also look for signs that a candidate engages with emerging niches and independent analysis ecosystems, including resources centered on expert prediction market analysis, because strong researchers tend to explore overlapping domains before they become mainstream.

Hiring Manager Tip: Ask what the candidate has changed their mind about recently. Real researchers update beliefs. Poseurs defend them.

Candidate Action Step: Keep a research journal with idea, rationale, test design, result, and next step. Review it monthly. The point isn't volume. It's building a feedback loop.

6. Risk Management and Portfolio Optimization Expertise

A quant who can generate signals but can't control risk is unfinished.

This skill often gets undervalued in hiring because it's less glamorous than alpha generation. In practice, it's one of the clearest answers to what skills separate a good quant from a great one. The strongest quants understand that a strategy's quality isn't just about expected return. It's also about exposure concentration, path dependency, correlation shifts, liquidity stress, and what happens when assumptions break at the same time.

Great quants think in distributions, not single outcomes

The best people in this area don't ask only, “Will this make money?” They ask, “What is this actually exposed to, and how does it fail?” That mindset changes portfolio construction, position sizing, and strategy combination.

Bridgewater, AQR, Winton, and multi-strategy firms with strong portfolio processes are often discussed as examples of institutions that treat risk as a design discipline. The cautionary counterexample is Long-Term Capital Management, which remains a reminder that advanced models can still collapse when tail assumptions prove too optimistic.

Good practice usually includes several layers:

- Multiple views of risk: Factor exposure, scenario analysis, concentration, and liquidity all matter.

- Stress thinking: Historical and hypothetical scenarios should both be part of review.

- Position discipline: Limits, budgets, and escalation rules prevent one idea from dominating the book.

A quant who treats risk as a reporting function will eventually get surprised by it. A quant who treats risk as part of research design usually sees the surprise earlier.

Hiring Manager Tip: Ask candidates to describe a profitable strategy they would reject on risk grounds. That reveals whether they can subordinate elegance to survivability.

Candidate Action Step: For every project, write a one-page risk memo before writing more code. Include key assumptions, likely failure modes, correlated bets, and conditions under which the strategy should be shut down.

7. Institutional Communication and Stakeholder Management

A quant can be right and still fail inside an institution.

That happens when the model logic isn't explained clearly, the uncertainties are hidden, or the team around the quant can't tell what decision should follow. Communication isn't separate from quant work. It determines whether the work gets funded, trusted, monitored properly, and integrated into actual portfolio decisions.

The model only matters if other people can act on it

Executives, portfolio managers, risk leads, investors, compliance teams, and engineers don't need the same explanation. Great quants know how to tailor the message without distorting the substance. They can explain assumptions, confidence levels, and operational implications in language each audience can use.

In scenarios requiring clear communication, many technically strong candidates underperform. They answer with jargon when a plain explanation is needed, or they present outputs without clarifying uncertainty. By contrast, senior research leaders and investment thinkers who influence institutions tend to make complex logic legible.

Useful communication habits include:

- State the decision first: What should the team do differently because of this work?

- Expose uncertainty: Confidence intervals are less important than honest limits and practical caveats.

- Document assumptions: Trust grows when people can inspect the reasoning.

Clear communication doesn't make a quant less technical. It makes the technical work usable.

Hiring Manager Tip: Ask the candidate to explain a model twice. Once for a quant peer, once for a non-technical risk committee member. The gap between those explanations is revealing.

Candidate Action Step: Take one past project and rewrite the summary for three audiences: a trader, a CTO, and a risk manager. That exercise builds institutional fluency fast.

8. Adaptability and Rapid Skill Acquisition in Evolving Technology

The field doesn't sit still. Great quants don't either.

Tools change, languages rise and fall, data sources expand, infrastructure shifts, and model development practices evolve. A quant who ties identity to a single language, workflow, or market regime usually gets slower over time. A quant who keeps learning stays valuable even as the environment changes.

The best quants keep rebuilding their toolkit

The profession has already moved through several major transitions, including broader adoption of Python and C++, heavier machine learning usage, and tighter integration between research, engineering, and production. The lesson isn't to chase every trend. It's to keep upgrading the stack where the upgrade solves a real problem.

Strong adaptability looks practical, not performative:

- Learning with purpose: New tools should connect to a real bottleneck or opportunity.

- Core plus frontier: Keep core math and coding strong while exploring adjacent methods.

- Fast assimilation: The ability to get useful quickly matters more than being early to every tool.

Candidates who adapt well usually leave evidence. They migrate projects to better architectures, pick up an unfamiliar library to solve a concrete issue, or move from notebook-heavy workflows to reproducible pipelines when the work requires it. They don't just collect buzzwords.

Hiring Manager Tip: Ask candidates to describe the last technical skill they had to learn under pressure and how they got productive. The method matters more than the topic.

Candidate Action Step: Pick one capability each quarter that directly supports your current quant path. It might be C++ performance tuning, temporal validation for ML, or market data pipeline design. Build a small project around it so the learning sticks.

8-Skill Comparison: Good vs Great Quants

| Item | Implementation complexity | Resource requirements | Expected outcomes | Ideal use cases | Key advantages |

|---|---|---|---|---|---|

| Advanced Mathematical and Statistical Modeling | Very high, requires advanced theory and careful calibration | Highly skilled researchers, numerical libraries, moderate compute | Rigorous, defensible models with quantifiable edges | Complex derivatives pricing, statistical arbitrage, proprietary alpha research | Precise risk quantification; potential for unique, hard-to-replicate strategies |

| Software Engineering and Systems Design Excellence | High, engineering discipline and production hardening needed | Significant infrastructure, low-latency hardware, experienced engineers | Reliable, scalable execution with low slippage | High-frequency trading, production trading platforms, large AUM execution | Robustness and scalability; reduces operational and execution risk |

| Machine Learning and AI Applied to Financial Markets | High, model design, validation, and deployment complexity | Large, high-quality datasets, GPU/cluster compute, ML specialists | Discovery of non-linear patterns and high-dimensional signals (with risk of overfit) | Predictive modeling, alternative data exploitation, adaptive strategies | Ability to process alternative/high-dim data and uncover subtle patterns |

| Deep Understanding of Market Microstructure and Liquidity Dynamics | High, requires granular data and specialized modeling | Tick/order-book data, execution systems, domain experts | Improved execution, lower transaction costs, practical strategy viability | Market-making, execution algorithms, latency-sensitive strategies | Practical edges in execution and liquidity capture; lower slippage |

| Intellectual Curiosity and Independent Research Capability | Medium, process-driven but less engineering overhead | Time, access to papers/data, collaborative networks | Continuous innovation and early discovery of novel signals | Exploratory research, new-signal discovery, cross-domain idea generation | First-mover discovery of alpha; sustained research-driven advantage |

| Risk Management and Portfolio Optimization Expertise | Medium–high, analytical and scenario modeling complexity | Historical data, stress-test frameworks, risk specialists | Controlled drawdowns and optimized risk-adjusted returns | Institutional portfolio construction, risk budgeting, stress testing | Limits catastrophic loss; enables scalable, disciplined capital deployment |

| Institutional Communication and Stakeholder Management | Low–medium, soft-skill complexity rather than technical | Time for presentation, documentation, interpersonal skills | Better buy-in, capital allocation, and smoother internal execution | Raising capital, persuading risk/compliance, leadership roles | Increased influence, resource access, and organizational alignment |

| Adaptability and Rapid Skill Acquisition in Evolving Technology | Medium, process and culture change more than single project | Time investment, learning resources, supportive culture | Faster adoption of useful tools and resilience to tech shifts | Teams facing fast-moving ML, infra, or data trends | Maintains competitiveness; enables early use of valuable technologies |

From Good to Great Building Your Quant Edge

The cleanest way to think about quant excellence is as a portfolio, not a checklist. That framing matters because firms often hire as if one spike will cover every weakness. It usually won't. A brilliant modeller who can't ship code creates bottlenecks. A fast engineer with weak statistical judgment scales bad ideas efficiently. A strong researcher who can't explain assumptions struggles to earn trust when it matters.

That's why what skills separate a good quant from a great one is the wrong question if it's interpreted too narrowly. There isn't one magic differentiator. There's a set of reinforcing capabilities that multiply each other: mathematical depth, software quality, applied ML judgment, execution realism, research independence, risk discipline, communication, and adaptability. The best quants build enough breadth to connect those pieces and enough depth to be exceptional in at least one or two of them.

For aspiring quants, the practical move isn't trying to become equally strong in everything at once. That leads to shallow competence. It's better to build a clear spike, then widen deliberately around it. A candidate with deep modeling ability should invest next in implementation and communication. A strong quant developer should deepen market intuition and statistical reasoning. A machine learning-heavy researcher should sharpen risk framing and execution awareness. The point is to become more complete over time.

For hiring managers, the same portfolio logic improves selection. Uniformly decent candidates often feel safe. They rarely become force multipliers. Stronger hiring comes from identifying people with real spikes plus evidence of connective tissue across adjacent skills. Can they move from theory to code? From code to production? From production to decision support? Can they explain trade-offs accurately? Can they keep learning as the environment changes? Those questions reveal long-term potential far better than prestige filters alone.

This is also where interview design matters. Too many quant hiring processes overweight puzzles and underweight work simulation. Firms get better signal when they test model judgment, debugging, communication, and risk reasoning in context. Candidates get a fairer shot too, because the process measures how they'd perform in the role rather than how well they rehearse canonical interview tricks.

The market doesn't reward quants for being impressive in isolation. It rewards people who can turn difficult ideas into repeatable outcomes under real constraints. That's the key edge. Great quants don't just know more. They integrate more, faster, with better judgment.

Nexus IT Group helps firms hire the kind of quantitative, engineering, and AI talent that can perform under real production and market pressure. Teams building research platforms, trading systems, data pipelines, or specialist quant groups can work with Nexus IT Group to find candidates who bring both technical depth and practical fit.